Debunking Gold Manipulation

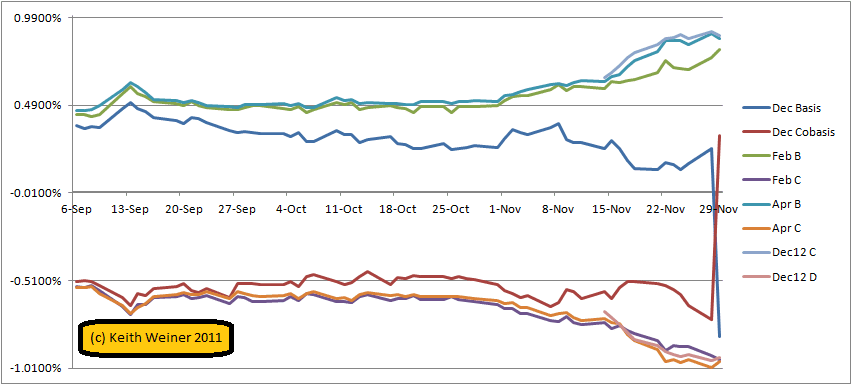

Yesterday [Nov 29, as I wrote this on Nov 30], the December gold contract moved sharply into backwardation (it happened in silver also, but let’s focus on gold). This means that one could sell physical and simultaneously buy December to make a profit (please see the graph).

So let’s look a little deeper. December basis fell massively, and cobasis rose equally. The other months were unaffected.

Basis is the profit you would make to carry gold (buy spot and simultaneously sell a future). Basis = Future (bid) – spot (offer).

When it falls, it could be either a falling bid on the future or a rising offer on spot.

Cobasis is the profit you would make to de-carry gold (sell spot, buy future). Cobasis = Spot (bid) – future (offer). When it rises, it could be a rising bid on spot or a falling offer on the future.

For both to be true, it means either spot is rising or the future is falling. But since the bases in the other months did not exhibit this behavior, it rules out spot rising, and that means that the Dec gold future fell.

What could cause a gold future to fall relative to spot and the other future months? Put it another way, what would cause unbalanced selling of a future relative to other months? One hint is that the February contract deviated from the other farther-out contracts and had a rising basis and falling cobasis. February moved higher in price relative to other contract months.

This is caused by the contract “roll” as naked longs must sell their Dec futures and if they wish to remain long gold, buy a farther-out contract (i.e. February). This action, especially if it happens en masse, would sharply press the bid down in Dec.

It is equally interesting that the offer is falling too. What of the conspiracy theory that the banks have massive naked short positions?

If they did, they would be forced to buy them back as the contract expired. This would lift the offer on the future. In that case, the cobasis would be falling, the opposite of what is occurring.

This is the basis (no pun intended) of how one would go about debunking the allegations that the precious metals markets are manipulated by massive short-selling of futures.

As a side note, the spread between the Dec 2011 contract and Feb 2012 contract also widened sharply. It had been falling since late October, accelerating in November.

Yesterday, it was possible to buy Dec (at the offer) and sell Feb (on the bid) for a profit of almost $6 an ounce. While this is too small to be actionable if you have to pay commissions and fees and storage for two months (about $8.50 for a retail account), it’s telling.

Trackbacks & Pingbacks

[…] and silver manipulation several times, in chronological order: Debunking Gold Conspiracy Theories Debunking Gold Manipulation Open Letter to Ted Butler NB: In this article, we used gold market data. The same analysis applies […]

[…] have written in the past about gold and silver backwardation (Debunking Gold Manipulation, Decline and Fall of Silver Backwardation, Is Gold Backwardation Now Permanent). The gist is that […]

Comments are closed.