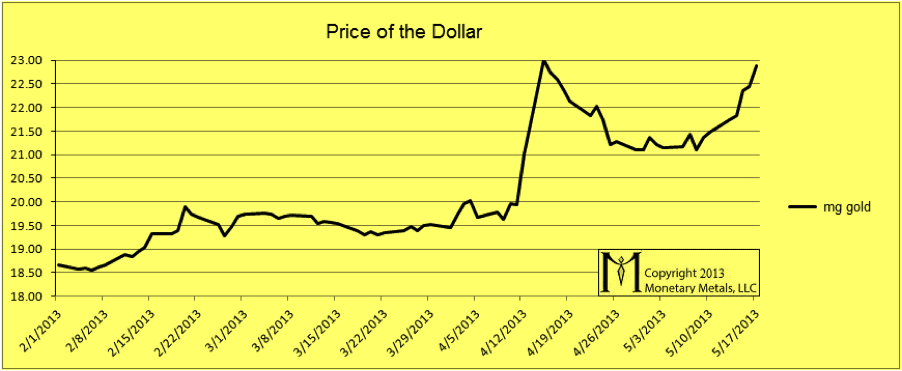

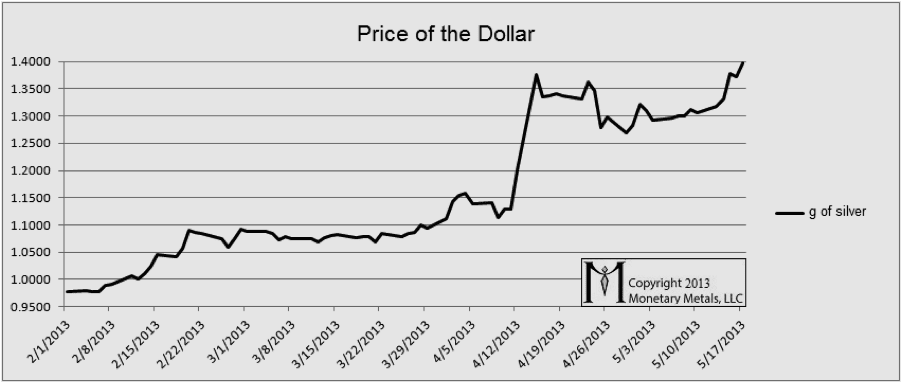

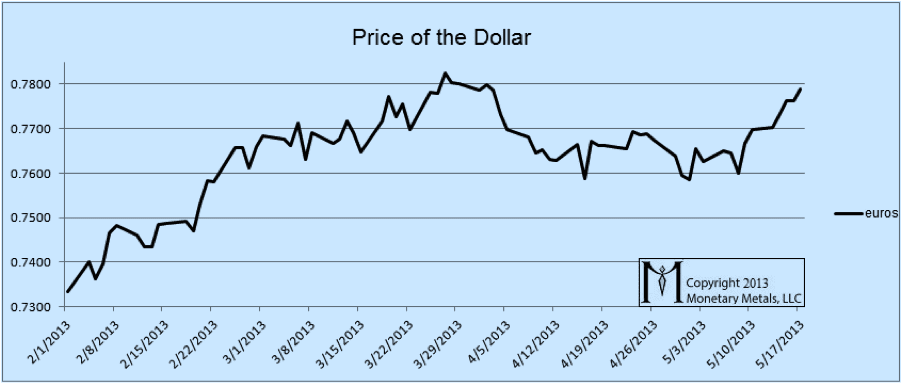

Let’s take a look at a few graphs of the dollar, from Feb 1, 2013 through Friday May 17, 2013. Yes, I said graphs of the dollar. I’ve priced the dollar in gold first (of course), then silver, the euro, and even the yen. The pattern is obvious. The dollar is going up.

I did not show copper, lumber, or wheat though they show the same trend. These commodities are not money, of course.

My point is simple. It’s not gold that is going anywhere. In past articles, I’ve used the analogy of measuring a steel ruler using rubber bands. Using the dollar to measure gold is like that. In this article I show that it’s not just gold, but silver, other currencies, and commodities. The dollar is rising now matter how we measure it.

The question not to ask is: “how are they manipulating gold?” The question is: “why is the dollar rising?”

To answer that, we first have to understand why the dollar had been going down. Most would say that it’s because the Fed has been “printing” and increasing the quantity of dollars. If that is so, then why would the dollar ever rise, as it has before (e.g. in the 1980’s), and as it is doing now? The Fed cannot and does not “un-print” dollars. This stock explanation is not satisfactory.

In one word, the answer is: arbitrage.

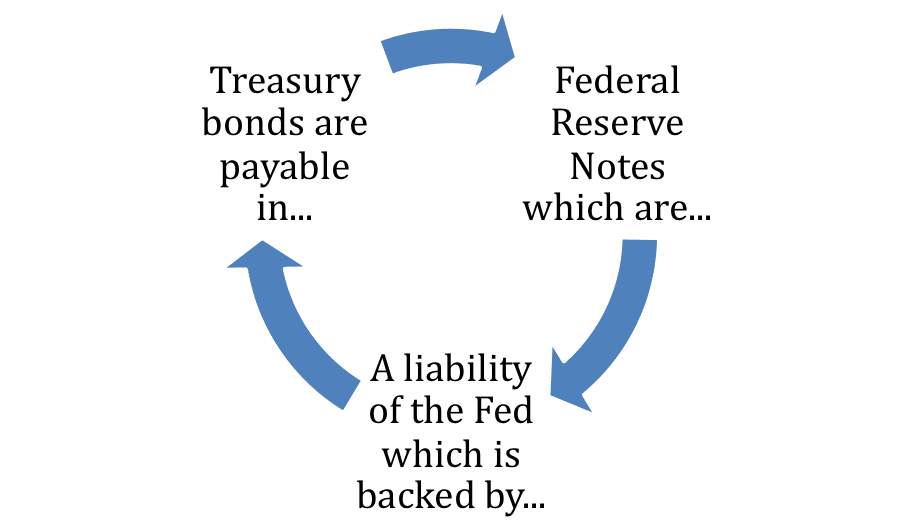

Let’s take a step back and look at the Treasury bond. The government pays for net expenses above tax revenues by borrowing. To borrow money, the Department of the Treasury sells bonds. This is an important aspect of our current form of government, as voters have demanded far more government expenditures than they are willing or able to pay for via taxes. In this aspect, the Treasury bond is a tool of fiscal policy, or spending, and cash flow to pay for it.

There is another aspect to the Treasury bond. It is the key asset of our monetary system. It is the asset on the Fed’s balance sheet (increasingly, post 2008, there are also mortgage bonds) to back its liabilities. The liability of the Fed is the Federal Reserve Note, commonly called the dollar. The Treasury bond is also a significant backing for the liabilities of commercial banks, pension funds, annuities, and insurance funds. Finally, the Treasury bond is used as collateral to enable borrowing.

The monetary system today is entirely based on credit, and the Treasury bond is the base of it. The peculiar characteristic, one could even say the shabby little secret, is that the Treasury bond is payable in dollars but the dollar is the liability of the Fed which is backed by the asset of the Fed which is … the Treasury bond. It’s circular and self-referential.

People often use the shorthand of saying that the Fed is “printing” dollars. It is actually borrowing them into existence and lending them. It is true that there is no actual lender. The Fed has sole discretion to create these dollars, unlike any normal bank, that must persuade a saver to deposit his capital in the bank. The Fed’s expansion of credit involves no saver. The Fed’s credit is counterfeit.[1]

The dollars appear ex nihilo at the Fed, and they use them to buy an asset, basically a bond, or to otherwise lend. Thus the Fed creates both a liability and an asset in this process. If the value of its assets should ever fall significantly, the market will not accept the Fed’s liability—the dollar—at face value. When gold owners refuse to bid on the dollar, the dollar will collapse.

Let’s get back to arbitrage. If a bank borrows money from the Fed, they will use it to buy an asset or lend it to a third party who will. This is an arbitrage. The short leg is the loan from the Fed, and the long leg is the asset purchased. As with all arbitrages, it will act as a force to pull the two values towards one another. Market price is always pulled down by the short leg, and pushed up by the long leg.

In the case of all borrowing from the Fed, the short leg is the dollar itself. I define arbitrage as the act of straddling a spread in the markets.[2] The arbitrager is often trying to profit from the interest rate spread directly, as in borrowing from the Fed at the discount rate and buying a Treasury bond that offers a higher yield.

Another strategy is to try to profit from a change in the spread, as in borrowing dollars to buy gold. In this case, if the dollar price falls, this will be a profitable trade. This is a weaker arbitrage than buying a bond, as gold does not have a yield.

As I noted above, the very act of arbitrage pulls down the price of the short leg and in the case of borrowing from the Fed the short leg is always the dollar. Whether a bank borrows dollars, to buy Euros and from there to buy Greek government bonds; whether it lends to a hedge fund to buy gold; or whether it lends to a consumer to buy a home, the dollar is pulled down. On the other side of the trade, these assets are pushed up.

This, rather than the rising quantity of dollars, explains the falling value of the dollar. And now, recently, the dollar has been rising. The logical explanation is that these trades are being unwound, either voluntarily or under duress. My definition of deflation is a forcible contraction of credit. It is not the shrinking number of dollars (if the number is even shrinking). It is the closing of innumerable positions, by the opposite arbitrage. Previously it was sell dollar / buy asset. Now it is buy dollar / sell asset.

Gold is the most liquid asset. Its bid-ask spread does not widen much when large quantities are sold on the bid or bought at the offer. In contrast, the bid in other assets can drop precipitously in times of crisis. They are hardest to liquidate precisely at the time when one must sell. In some extreme cases, the bid can be withdrawn altogether. Though the spread does not widen in gold, heavy selling does push down the bid on gold. Market makers will then pull down the offer to maintain a consistent spread.

Being the most liquid, gold is the most sensitive. It is the first asset, the “go to” asset to sell when a balance sheet is under stress. Gold therefore has the least lag in response to a change in the monetary system. Compare to real estate, where due diligence alone could take weeks or months. Additional inertia comes from how properties are valued: by looking at recent comparable deals. Real estate would not be the first asset that a bank or fund would want to sell, due to several factors including long closing time, wide bid-ask spread, and high costs to sell such as sales commissions and attorneys. In real estate, there are no market makers. The offer can remain high even with the bid plunging, as the typical holder of real estate is not willing to sell at a loss and holds out for a number that covers all costs and fees and allows an exit at a profit.

Equities are usually liquid, closer to gold than to real estate in this regard. However, for the past few years, there have been many flash crashes. In a flash crash, the bid drops to $0.01 for a brief moment, and typically at least one market sell order is filled far below the “normal” price for the stock. These flash crashes prove that there are serious problems, that there are structural cracks beneath the surface.

An important principle to keep in mind is that in times of stress or crisis, it is always the bid and never the offer that is withdrawn. While there have been a few flash smashes (an amusing term) it is not a coincidence that these are vastly outnumbered by the flash crashes. This is because stress and crisis always come with a need for liquidity to pay debts that cannot be rolled over, margin calls, or to be flexible and agile. In bad times, people prefer to own a more marketable asset compared to one that is less marketable. They especially prefer to own the asset that is the unit of account for their balance sheet.

By definition, there is no risk to holding dollars if your balance sheet is denominated in dollars, and your liabilities are in dollars. This is the reason for the so-called “flight to safety” for the “risk-off asset”. You are not making, nor losing, money when you hold dollars. On gold denominated books, holding dollars is quite risky, of course.

Going back to the falling dollar, as the interest rate falls the discount factor used for an enterprise’s future earnings also falls. The same $1 in earnings in 2023 is worth more at a discount of 3% annually vs. 6% ($0.74 vs. $0.56). The result is rising stock prices.

In addition, the “animal spirits” of John Maynard Keynes have been set loose. Most people hold the false theory about the quantity of money and its impact on the price of everything, and it is quite popular to believe that this means stock prices can only rise. Proponents of this theory should look at Japan. In any case, deprived of other means of obtaining a yield (i.e. in the bond market), they must do something. People know the dollar is falling, though they attempt to measure it by looking at the rate by which consumer prices, measured in dollars, rise. They should be looking at the rate at which the dollar, measured in gold, is falling.

Right now, everyone is on the same side of the trade: long equities. This is dangerous because when it reverses, the market may not find a bid for quite a distance down. In a normal market, it is the short sellers who make the bid. By the indications I can see, those who have attempted to short this market have capitulated by now.

In Part II (free registration required), we consider why stocks are rising in this depressed economy, and look at the abyss we are now rapidly approaching.

[1] My definition of inflation is an expansion of counterfeit credit, discussed in this paper: http://keithweinereconomics.com/2012/01/06/inflation-an-expansion-of-counterfeit-credit/

[2] I define and discuss in my dissertation: A Free Market for Goods, Services, and Money

Very nice article!

Interesting article.

The Fed has been all kinds of garbage the past few years incl. mortgage backed securities and have swapped treasuries for all kinds of troubled assets. What happens if the troubled assets default? Will the banks that got the treasury paper in exchange for the trouble assets just keep it since the troubled assets are worth zilch? And doesn’t that tear a hole in the balance sheet of the Fed if the banks would sell the treasuries back to them? The only way the Fed could pay for that would be to monetize more debt trough the treasury to print dollars to purchase the old treasury paper.

Do you think it is possible that the Fed could go bankrupt? If the Fed would go bust, what would happen to the dollar in that case?

schmidh: thank you.

petter: I think eventually the Fed will be bankrupt, when their assets collapse but their liabilities of course remain. Read on in Part II… :)