Falling Interest Rates Destroy Capital

I have written other pieces on the topic of fractional reserve banking and duration mismatch, which is when someone borrows short-term money to lend long-term and how falling interest rates actually encourage duration mismatch. Falling interest rates are a feature of our current monetary regime, so central that any look at a graph of 10-year Treasury yields shows that it is a ratchet (and a racket, but that is a topic for another day!). There are corrections, but over 31 years the rate of interest has been falling too steadily and for too long to be the product of random chance. It is a salient, if not the central fact, of life in the irredeemable US dollar system, as I have written.

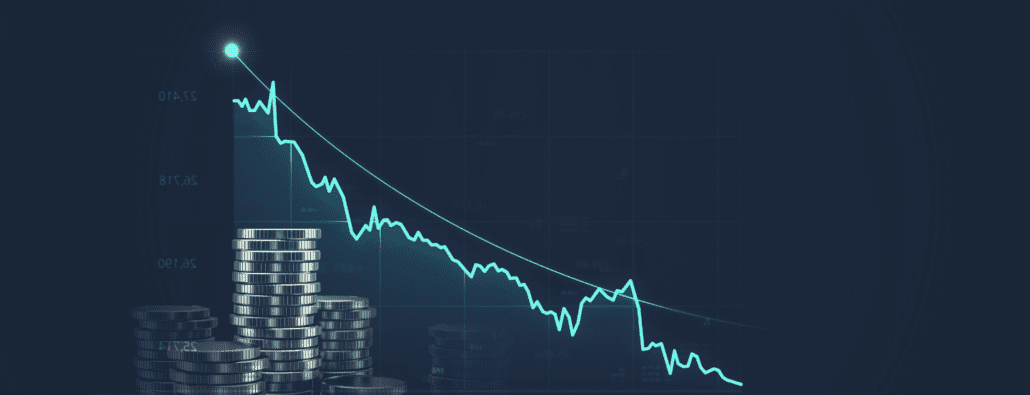

Here is a graph of the interest rate on the 10-year US Treasury bond. The graph begins in the second half of July 1981. This was the peak of the parabolic rise interest rates, with the rate at around 16%. Today, the rate is 1.6%.

Pathological Falling Interest Rates

Professor Antal Fekete introduced the proposition that a falling interest rate (as opposed to a low and stable rate) causes capital destruction. But all other economists, commentators, and observers miss the point. It is no less a phenomenon for being unseen. In early 2008, a question was left begging: how could a company like Bear Stearns which had strong and growing net income collapse so suddenly?

Here is Bear’s five-year net income and total shareholder’s equity:

Year

2003

2004

2005

2006

2007

Income

$1.156B

$1.345B

$1.462B

$2.054B

$0.233

Equity

$7.47B

$8.99B

$10.8B

$12.1B

$11.8B

Isn’t that odd? Even in 2007, Bear shows a profit. And they show robust growth in shareholder equity, with only a minor setback in 2007.

And yet, by early 2008 Bear experienced what I will call Sudden Capital Death Syndrome. JP Morgan bought them on Mar 16, for just over $1B. But the deal hinged on the Fed taking on $29B of Bear’s liabilities, so the real enterprise value was closer to $-19B.

Obviously, Bear’s reported “profit” was not real. And neither was their “shareholder’s equity”. I think it something much more serious than just a simple case of fraud. Simple fraud could not explain why almost the entire banking industry ran out of capital at the same time, after years of reporting good earnings and paying dividends and bonuses to management.

Also, other prominent companies were going bankrupt in 2008 and 2009 as well. These included Nortel Networks, General Growth Partners, AIG, two big automakers.

I place the blame for Sudden Capital Death Syndrome on falling interest rates. The key to understanding this is to look at a bond as a security. This security has a market price that can go up and down. It is not controversial to say that when the rate of interest falls, the price of a bond rises. This is a simple and rigid mathematical relationship, like a teeter-totter.

A bond issuer is short a bond. Unlike a homeowner who takes out a mortgage on his house, a bond issuer cannot simply “refinance”. If it wants to pay off the debt, it must buy the bonds back in the market, at the current market price.

Let’s repeat that. Anyone who issues a bond is short a security and that security can go up in price as well as go down in price.

Everyone understands that if a bond goes up, the bondholder gets a capital gain. This is not controversial at all. Nor is it controversial to say that there are two sides to every trade. And yet it is highly controversial—to the point of being rejected with scorn—that the other side of the trade from the bondholder incurs the capital loss. It is the bond issuer’s capital that flows to the bondholder. To reject this is to say that money grows on trees.

We won’t explore that any further; money does not grow on trees! Instead, we will look at this phenomenon of the capital loss of the bond issuer from several angles: (1) Hold Until Maturity; (2) Mark to Market; (3) Two Borrowers, Same Amount; (4) Two Borrowers, Different Amounts; (5) Net Present Value; (6) Capitalizing an Income; (7) Amortization of Plant; and (8) Real Meaning of an Interest Rate.

Hold Until Maturity

There is an argument that the bond issuer can just keep paying until maturity. While that may be true in some circumstances, it misses the point. When one enters into a position in a financial market, one must mark one’s losses as they occur, no matter than one may intend to hold the position until maturity. How would a broker respond in the case of a client who shorted a stock and the stock rose in price subsequently? Would the broker demand that the client post more margin? Or would the broker be sympathetic if the client explained how the company had poor prospects and that the client intended to hold the short position until the company’s share price reflected the truth?

Mark to Market

The guiding principle of accounting is that it must paint an accurate and conservative picture of the current state of one’s finances. It is not the consideration of the accountant that things may improve. If things improve, then in the future the financial statement will look better! In the meantime, the standard in accounting (notwithstanding the outrageous FASB decision in 2009 to suspend “mark to market”) is to mark assets at the lower of: (A) the original acquisition price, or (B) the current market price.

There ought to be a corresponding rule for liabilities: mark liabilities at the higher of (A) original sale price, or (B) current market price. Unfortunately, the field of accounting developed its principles in an era where a fall in the rate of interest from 16% to 1.6% would have been inconceivable. And so today, liabilities are not marked up as the rate of interest falls down.

Refusing to put ink on paper does not change the reality, however. Closing one’s eyes does not prevent one from falling into a pit on the path in front of one’s feet. The capital loss is very real, as we will explore further below.

Two Borrowers, Same Amount

Let’s look at two hypothetical companies in the same industry, pencil manufacturing. Smithwick Pen sells a 20-year $10M bond at 8% interest. It uses the proceeds to buy pencil-manufacturing equipment. To fully amortize the $10M over 20 years, Smithwick must pay $83,644 per month.

The rate of interest now falls to half its previous rate. Barnaby Crayon sells a 20-year $10M bond at 4%. Barnaby buys the same equipment as Smithwick and becomes Smithwick’s competitor. Barnaby pays $60,598 per month to amortize the same $10M debt. Is it correct to say that both companies have identical balance sheets? Obviously Barnaby will have a better income statement. This is because it has a superior capital position, and this should be reflected on the balance sheets. It certainly is not because of its superior product, management, or marketing.

Let’s look at this from the perspective of the capital position: the present value of a stream of payments. Obviously, at 4% interest the monthly payment of $60,598 has a present value of $10M (otherwise we made a mistake in the math somewhere). But what is the value of an $83,644 monthly payment at the new, lower rate of 4%? It is $13.8M. Smithwick’s has just experienced the erosion of $3.8M of capital! This is reflected in reality, by the uncontroversial statement that it has a permanent competitive disadvantage compared to Barnaby. Barnaby can undercut Smithwick and set prices wherever it wishes. Smithwick is helpless. Most likely, Barnaby will eke out a subsistence living, until the rate of interest falls further. When Cromwell Writing Instruments borrows money at 2%, then Smithwick will be put out of its misery. And Barnaby will be forced into the untenable position it had previously placed Smithwick.

It should be noted that the longer the bond maturity, the bigger this problem becomes. For example, if this were a 30-year bond, then Smithwick would take a $5.4M hit to its capital if interest rates were 8% when it issued the bond and then fell to 4%.

Two Borrowers, Different Amounts

This is not the only way that a competitor can exploit the capital loss of a company who made the mistake of borrowing at a too-high interest rate. Let’s look at the case of Poddy Hoddy Hotel and Casino. Poddy sells a 20-year $100M bond at 8%, and has a monthly payment of $836K. It builds a nice hotel and casino with bars, a restaurant, a pool, and a few jewelry stores.

A short while later, Xtreme Hotels sells a $138M bond at 4%, and has the same monthly payments. The extra $38M goes into a second pool with a swim-up bar, another restaurant that is themed based on the Galapagos Islands, bigger and more opulent retail stores, and a spiral glass elevator to take guests up to their rooms while enjoying the breathtaking 270-degree views of the city.

Which hotel will consumers prefer?

The Poddy Hoddy Hotel may have been planned based on accurate market research that showed real demand for such a hotel in that location. Unfortunately, the falling interest rate has undermined it. Its investors will likely lose money.

The Xtreme Hotel, on the other hand, is probably a mal-investment. It is likely a project for which there is no real demand. But the falling interest rate gives a false signal to the entrepreneur to build it. Of course, the Xtreme won’t be the one to experience Sudden Capital Death Syndrome first. That fate will befall Poddy. Xtreme’s turn will come later, at a lower interest rate.

With Smithwick, one might argue that it can pay off its bond in the 20 years it originally expected, so it has not experienced a loss. But in fact, there is a loss even from this angle. Smithwick is paying off its 8% bond at $83,644 per month. But the rate of interest is now 4%, which should be a payment of $60,598. The accurate way to look at this is that Smithwick is paying off a market-rate bond plus a penalty of $23,046 for every month remaining before the bond is fully amortized.

With Poddy Hoddy, one might similarly argue that it can pay off its bond as planned, so it has not taken a loss. But the loss here is even clearer. By borrowing $100M at a rate that was too high, it has effectively dissipated the extra $38M that its competitor, Xtreme, put to good use. It will pay for this waste every month for 20 years (or until it goes bankrupt).

By not marking the losses at Smithwick and Poddy, the accountants are not doing these companies or their investors any favors. In the short run, these companies may declare “profits” and based on that pay dividends to investors and bonuses to management. But sooner or later, they will meet Barnaby and Xtreme who will deal the coup de grace of Sudden Capital Death Syndrome.

Net Present Value

As alluded above, one can calculate the Net Present Value (NPV) of a stream of payments. First, let’s look at the formula to calculate the present value of a single payment is:

![]()

It should be obvious that the present value of a payment is lower the farther into the future it is to be made. One does not value a payment due in 2042 the same as a payment to be made next year. What is not so glaring is that the value is lower for higher rates of interest. A $1000 payment due next year is worth $909 if the rate of interest is 10%, but $990 at 1%. This difference is amplified due to compounding. At 10 years, the payment is worth $385 at 10% versus $905 at 1%.

The NPV of a stream of payments is the sum of the value of each payment. The value of a $1000 payment made annually for 20 years is $9818 at 8% interest. That same payment at 4% has an NPV of $13,590, a 38% increase.

It is important to emphasize that while the bond issuer’s monthly payment is fixed based on the amount of capital raised and the interest rate at the time, the NPV of its liability must be calculated at the current rate of interest. The market (and the universe) does not know nor care what bond issuer’s entry point was. Objectively, all streams of payments of $1000 per month have the same value at a given maturity and current interest rate, regardless of the original rate.

Capitalizing an Income

Let’s look at this from yet another angle. An income can be capitalized, and the purpose of capital is to produce an income. Professor Antal Fekete wrote:

“Suppose you are a worker taking home $50,000 a year in wages. When your income-flow is capitalized at the current rate of interest of, say, 5 percent, you arrive at the figure of $1,000,000. The sum of one million dollars or its equivalent in physical capital must exist somewhere, in some form, the yield of which will continue paying your wages. Capital has been accumulated and turned into plant and equipment to support you at work. Part of your employer’s capital is the wage fund that backs your employment. Assuming, of course, that no one is allowed to tamper with the rate of interest.” [Emphasis in the original]

“Suppose for the sake of argument that the rate of interest is cut in half to 2½ percent. Nothing could be clearer than the fact that the $1,000,000 wage fund is no longer adequate to support your payroll, as its annual yield has been reduced to $25,000. This can be described by saying that every time the rate of interest is cut by half, capital is being destroyed, wiping out half of the wage fund. Unless compensation is made by adding more capital, your employment is no longer supported by a full slate of capital as before. Since productivity is nothing but the result of combining labor and capital, the productivity of your job has been impaired. You are in danger of being laid off ? or forced to take a wage cut of $25,000.”

Without capital, human productivity is barely enough to produce a subsistence living. Without tools, one is obliged to work long hours at back-breaking tasks in order to have a meager meal, some sort of clothing, and something to keep the rain off one’s head. Capital destruction is the process of moving backwards towards a time where one worked harder to obtain less.

As described earlier, when the rate of interest falls, it erodes the capital of every bond issuer. If one looks at this capital as being the wage fund (or part of it is the wage fund), then the bond issuer can no longer afford to pay its employees the same wage. If it does continue the same wage anyway, it will eventually suffer the consequences of running out of capital.

Amortization of Plant

Now let’s consider the concept of amortizing equipment and plant at Smithwick Pen. Smithwick borrows $10M to buy equipment. Out of its revenues, it must set aside something to amortize this over the useful life of the equipment, which is 20 years in our example. This set-aside reduces net income; it is not profit but capital maintenance assuming the company intends to remain in business after the current generation of equipment and plant wears out.

How much should it set aside every month? This is the inverse of the NPV calculation. We are now interested in the current monthly payment to arrive at a fixed sum at a future point in time (as opposed to the present value of a stream of fixed payments). The lower the rate of interest, the more Smithwick must set aside every month in order to reach the goal by the deadline. To understand this, just look at what Smithwick must do. Each month, it puts some money into an interest-bearing account or bond. Even if it chooses the longest possible maturity for each payment (i.e. the first payment is put into a 20-year bond, the next into a 19-year 11-month bond, etc.) it is clear that if interest rates are falling then each payment must increase to compensate. Smithwick’s profits are falling with the rate of interest!

If Smithwick persists in setting aside every month what it initially calculated when it purchased the pencil-making equipment, it will have a shortfall at the end, when it needs to replace the equipment.

Real Meaning of an Interest Rate

Let’s consider what it really means to have a high or a low rate of interest. I propose to do reductio ad absurdum. We will look at two cases (which would be pathological if they occurred) to make the point clearer.

The first case is if the rate of interest is 100%. This means that a $1000 payment one year from today is worth ½ of the nominal value, or $500 today. A payment due in two years is worth $250 today, etc. At this rate of interest, for whatever reason, “future money” is worth very little present money. In other words, the burden experienced by the debtor is a small fraction of the nominal value of the debt.

The second case is if the rate of interest is zero. This means that a $1000 payment due one year from today or 100 years from today is worth $1000 today. At this rate of interest, for whatever reason, future money is worth every penny of its nominal value today. There is no discount at all, not for the loss of use of the money in the meantime, not for the risk, not for currency debasement. In other words, the burden experienced by the debtor is the full nominal value of the debt.

Again, to emphasize, one must use the current market rate of interest not the rate of interest contracted by the borrower at the time of the bond issuance.

The lower the rate of interest, the more highly one values a future payment. The higher the rate of interest, the more highly one discounts a future payment. These statements are true whether one is the payer or the payee. The payer and payee are just parties on opposite sides of the same trade.

Irving Fisher, writing about falling prices (I shall address the connection between falling prices and falling interest rates in a forthcoming paper) proposed a paradox:

“The more the debtors pay, the more they owe.”

Debtors slowly pay down their debts and reduce the principle owed. This would reduce the NPV of their debts in a normal environment. But in a falling-interest-rate environment, the NPV of outstanding debt is rising due to the falling interest rate at a pace much faster than it is falling due to debtors’ payments. The debtors are on a treadmill and they are going backwards at an accelerating rate.

How apropos is Fisher’s eloquent sentence summarizing the problem!

http://www.wikinvest.com/stock/Bear_Stearns_Companies_(BSC)#History

http://www.wikinvest.com/stock/Bear_Stearns_Companies_(BSC)/Data/Balance_Sheet#Balance_Sheet

http://www.professorfekete.com/articles/AEFLaborLeaders.pdf

http://fraser.stlouisfed.org/docs/meltzer/fisdeb33.pdf

Make sure to subscribe to our YouTube Channel to check out all our Media Appearances, Podcast Episodes and more!

Additional Resources for Earning Interest on Gold

If you’d like to learn more about how to earn interest on gold with Monetary Metals, check out the following resources:

In this paper we look at how conventional gold holdings stack up to Monetary Metals Investments, which offer a Yield on Gold, Paid in Gold®. We compare retail coins, vault storage, the popular ETF – GLD, and mining stocks against Monetary Metals’ True Gold Leases.

The Case for Gold Yield in Investment Portfolios

Adding gold to a diversified portfolio of assets reduces volatility and increases returns. But how much and what about the ongoing costs? What changes when gold

Trackbacks & Pingbacks

[…] of the many problems with falling interest rates is that it becomes near impossible to outpace inflation with your […]

[…] of the many problems with falling interest rates is that it becomes near impossible to outpace inflation with your […]

Лучшие фильмы!

Смотрите фильмы лидеры проката

Comments are closed.