Monetary Metals Silver Headfake Report: 22 June, 2014

Something extraordinary occurred this week. On Wednesday, the Fed made a routine announcement. That day, the price of silver was rising, but not out of the normal. Fireworks began on Thursday, and in 6 hours, the price of silver skyrocketed by 5%.

We have never before changed the headline or format of the Supply and Demand Report. However, it is warranted under the present circumstances.

The Fed’s announcement was mundane. It will continue tapering its bond purchases, from $45B monthly to $35B. It will continue its low interest rate policy. It cut its growth forecast. This was all expected except, arguably, the cut in the forecast.

Some pinned this move on the unwinding of the Chinese commodity finance scheme. That unwind will involve selling metal and buying futures. The impact of this is a rising basis, but probably not a rising price.

Many said that that the Fed was to blame (or credit). One commentator even said that gold had now become an inflation hedge. Apparently it wasn’t last week, but now it is. We respectfully suggest that he step back and take a deep breath.

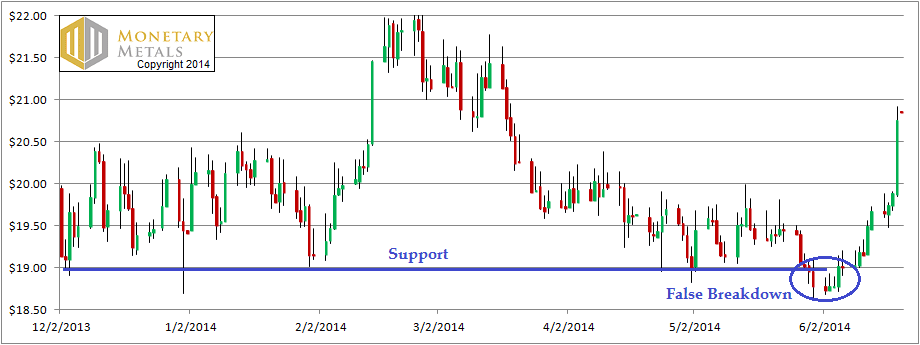

Looking at a price chart, the action is pretty obvious. This candlestick chart is not the standard chart format we normally use in this Report.

Silver Chart

The blue line shows support around $19, going back 7 months. In the last few days of May, the silver price broke below that line. But by June 10, the price broke out through the line sharply. The breakdown at the end of May was a false breakdown.

Thursday’s price move also drove above the 100-day and 200-day moving averages (not shown). In March, silver had dropped below both averages, which have been falling for a long time.

There are other ways of analyzing the silver price chart, though that is not our focus here. No matter how you look at the price chart, the sharp spike in the silver price appears very bullish.

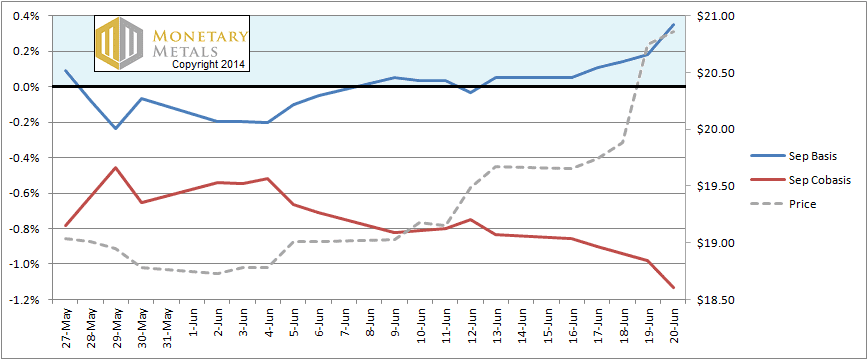

We therefore want to look at another chart, showing the silver basis and cobasis. Think of them as measures of abundance and scarcity, respectively.

We’re going to skip the gold graph this week. Silver did what gold did, and more.

The Silver Basis and Cobasis and Price

Normally in the Report, we include a long period of time (e.g. October 2013 through June 2014, or 8+ months). This week, we zoom in to see detail. The graph begins on May 27, which is when the silver price broke down below $19. We can see a decrease in abundance (blue line) and an increase in scarcity (red line) through June 4.

Then the price begins to rise, and with it abundance. Scarcity drops. The basis and cobasis made large moves. For clarity, the zero line has been drawn in heavy black and the region above is shaded light blue.

From its low, the basis rises from -0.24% to +0.35%. The basis is the carry you can earn in silver. To carry is to buy the metal and sell a futures contract. The annualized profit on a trade with less than 3 months to maturity is 35 now basis points. That’s a lot. The 3-Month Treasury bill, for comparison, earns 2 basis points.

So what is this telling us?

Silver futures were heavily bought. While there are other buyers of futures (e.g. electronics manufacturers who plan for their needs in advance), such a sharp change is generally driven by speculators.

Why do speculators buy silver futures? They anticipate a rise in the price, from which they hope to profit. They can drive the price up with their buying, as we see yet again this week, but they don’t tend to sustain big price moves. When we say they anticipate, we really mean front-run. They are expecting, rightly or wrongly, that real physical demand is coming. They want to buy ahead of it, and sell into it.

This week, their expectations of hoarders changed significantly. Speculators now believe demand from hoarders will rise.

Hoarders are, in many ways, the opposite of speculators. They do not use leverage. They do not buy with the intention of selling soon. They are not necessarily thinking of profits when they buy. They are thinking about preserving wealth, perhaps for the next generation. They take metal out of the market for the long term.

It is the hoarders that speculators are trying to front-run.

Clearly, speculators this week expect a growing demand to hoard. That’s probably what that analyst meant when he said that gold became an inflation hedge this week.

The speculators may even turn out to be right. It is possible that real demand for physical metal, which does not exist in the market today, will begin ramping in the coming week. Perhaps this time the speculators know something that the hoarders don’t yet know. There is a first time for everything, and this could be the first time that speculators jumped the gun on a Fed announcement and beat the hoarders to buy at the last of the lower prices.

We wouldn’t bet on it.

And that’s the whole point, isn’t it? The silver longs are indeed betting on it. When they use 4:1 (or greater) leverage to buy a silver future at $20.86, they are hoping to be able to sell it soon at $21.86, $31.86, or $186.

I had a brief twitter exchange with someone this week. He said that the basis is not a good indicator of timing. He added that the there was a collapse of the cobasis in January followed by a long rally.

He is correct that the basis does not give timing. It is entirely possible that the silver price chart now looks so tempting, that more traders will pile in to the metal this week. However, he is not quite correct about the “long” rally. It lasted for about two weeks, and took the price from $19.15 to $21.89. By the end of March, half the gain had been given back, and by the end of April all of the gain was gone.

Let us all recall for a moment the long rally from August 2010, to April 2011. The silver price rose from $18 to $49. That was a long rally, in terms of time, over 8 months. More importantly, it was a long rally in terms of price action: 172%. In that long rally, by the way, we observed backwardation in contracts dated out to 2015. That simply is not the case today.

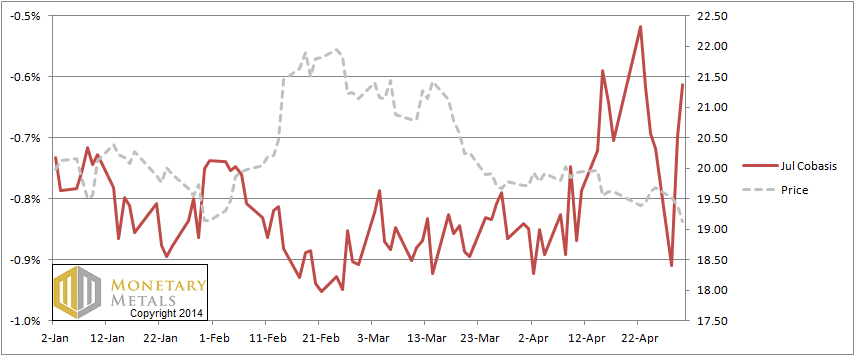

Here is a graph showing the basis graph from January and February of this year, overlaid with price.

The Silver Price and Cobasis Jan-Apr

This shows the basis for the July contract, which is around half a year from expiration in this time period. Being farther from expiry, it doesn’t yet undergo the higher volatility of the March and May contracts that we showed in the Reports of that time period. Being farther from maturity, it is not directly comparable. An apples-to-apples comparison shows that the drop is much bigger this month than it was in January.

There is a negative feedback in a rising price with rising basis. Silver is a monetary metal. This means that it’s unlike other commodities in that it is accumulated without any particular limit. The ratio of stocks to flows (i.e. inventories divided by annual mine production) is measured in decades for silver. For normal commodities, the ratio of stocks to flows is a few months—a fraction of one year’s production.

This means, among other things, that the supply of silver to the market need not come from the mines. All existing stocks of silver are potential supply, under the right conditions, and at the right price.

A rising basis combined with a rising price means that demand for futures is exceeding demand for metal. With rising prices, the demand for metal drops while the supply rises. Unlike in other commodities, existing inventories add to supplies.

With a high basis, the marginal demand for metal is to go into the warehouse, to go into carry trades. When the basis is rising, then warehousing is rising as well.

The problem is that, eventually, what goes into carry positions must eventually come out. The warehouse, formerly the marginal demand for metal, becomes the marginal supply. Down comes the price, perhaps more quickly than it went up.

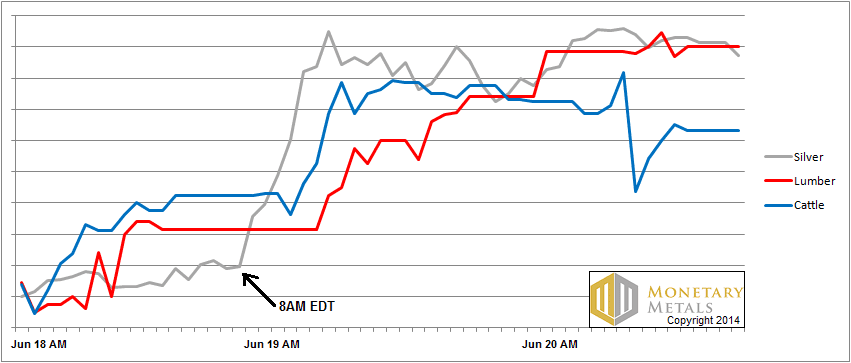

There is one final thing worth looking at. Commodities went up at the same time as silver. Here is a picture of the prices of silver, lumber, and cattle.

The Price of Silver, Lumber, and Live Cattle

Lumber and especially live cattle are not for hoarding. They are for consumption, and of course for speculating (everything is for speculating in the regime of zero interest). We would not expect hoarding demand for silver to coincide so neatly with rising real demand for wood and meat. But on the other hand, speculative demand for silver can perfectly coincide with speculative demand for wood, meat, and all sorts of other things. Why shouldn’t traders bet on a rising silver price and a rising beef price?

Whatever it may mean, that traders bought these three things at the same time, we doubt it is that demand for hoarding silver is on the rise. While it may be different this time, the most likely outcome is that silver speculators will drown in a deluge of metal coming to market.

This is a good opportunity to reiterate our long-standing advice. Never naked-short a monetary metal.

© 2014 Monetary Metals

Yellen downplayed the possibility of emerging inflation during the Fed announcement. Speculators are thinking that the Fed will try to keep real interest rates negative, and they are betting that hoarders will be buying commodities including gold and silver as inflation hedges.

Nice post Keith!

Always insightful and informative. Excellent reporting again Keith, thank you.

Thanks jtibbs and bleubelle.

limco: My point in this article is that quite a lot of people quite suddenly turned on the “inflation trade”. The suddenness of it is itself suspicious, and the lack of demand for physical metal is telling.

More broadly, is the question of what a falling interest rate does to prices. One theory, based on the quantity of money, predicts rising prices. I have proposed a different theory: http://keithweinereconomics.com/2013/12/28/the-theory-of-interest-and-prices-in-paper-currency/

HI There is a wide difference between the absolute value of the basis and the cobasis, i.e. 0.25 vs 1.2

What is the reason for this wide spread? is this due to a wide spread between the future bid and ask? If so what does this gap say about the demand for silver?

“[High stocks to flows] means, among other things, that the supply of silver to the market need not come from the mines. All existing stocks of silver are potential supply, under the right conditions, and at the right price.”

If the implication here is that silver will be dishoarded as the price rises, you are ignoring the very nature of silver as a monetary metal. It is axiomatic that as the dollar falls against silver, more silver will not come to market, but will go into hiding.

Thanks for the questions.

jfbastian:

basis = future(bid) – spot(ask)

cobasis = spot(bid) – future(ask)

The math dictates that if the bid-ask spread widens on either spot or futures, then that will cause either basis or cobasis to drop, depending on which spread and in which direction.

It does not, in itself, say something about demand if the spread is widening. It says something about liquidity. I have written a few articles touching on the issue of liquidity in silver, arguing that it is dropping.

mossmoon: If the basis is rising with the price, then that does mean that silver is being dishoarded. I agree with you that, in the end, price will be rising (likely exponentially) and it will be fueled by increased hoarding. But that will be a time of hugely negative basis, and positive-and-rising cobasis–backwardation. That day will come, but it is not this day.

Hello Keith, I appreciate your attempts to educate the public about this little studied (or at least little understood), aspect of the PM Markets. Some of us are visual, some are more verbal in their way of understanding things. Perhaps a visual of a chart of the basis/cobasis, which would predict prices rising would be helpful. You may have already done one for all I know but I haven’t seen it. What did the basis cobasis studies predict prior to the run up of silver to 49 last time?

Hello Kieth, Thanks for the wonderful insight. Have you looked at this basis/cobasis information for gold going back to the 2008 lows. Seems like the commercials were really short back then just like they are now, but somehow gold still rallied and more than doubled in 3 years. Did we have backwardation back then?