Monetary Metals Supply and Demand Report 26 July, 2015

For those who are speculating on the dollar—i.e. most people—there was good news this week. The dollar rose almost a milligram, to 28.3mg gold. That’s a big gain, and welcome news for those who keep all of their eggs in the one dollar basket, perhaps because they don’t want to risk any of it on pet rocks.

Yes, Jason Zweig at the Wall Street Journal actually said that. He couldn’t be more wrong—and yet he had a point. Wrong? Let me count the ways.

One, per his title, he compares gold to a pet rock. A pet rock is either a useless knickknack, or else a fraud that preys on the irrational psychology of people in crowds. Gold is honest money, and the extinguisher of debt. Just because governments have banned it from the monetary system, does not make it either useless or a fraud.

Two, he quotes a Barclays researcher saying that investors have become disillusioned with gold. Well, gold is not an investment. Even if one accepts the mainstream premise that gold is a commodity that you buy so you will make money—i.e. dollars—when it goes up, this is speculation. It is not investing. Our whole financial world is now stoned on the drug of zero interest rates. With no yield to be had, capital gain is all.

Three, he says to own gold is an act of faith. Boy is this backwards! To go all-in on the debt of bankrupt governments is the real act of faith. And that is what one does, if one holds dollars or euros or pounds, etc.

Fourth, he refers to inflation (by which he means rising prices) a few times. Gold purportedly has magical powers to fight inflation, but gold isn’t a “panacea” for it (straw man, much?) He later says gold is viewed as a hedge against inflation, but it does not go up as much as the alternatives (whatever those may be).

I could go on, but I will stop here. Despite the cornucopia of errors, there is an excellent point buried in Zweig’s blog post.

Suppose, as Zweig says, that everyone—or at least the current marginal gold trader—views gold as a speculative vehicle. In this view, it’s only useful to make bucks. Then, of course its price action is about as rational as the path of the planchette on a Ouija board. Everyone has the same price charts, and the same technical tools. Everyone can see the same trends. So when it is going up, it goes up. And when it is going down, it goes down.

Of course, this may temporarily describe market conditions. But it in no way objectively describes gold.

The price of gold dropped further this week, especially last Sunday night. We would guess that margin calls in China forced some liquidation. The price of silver did not drop as much, which is interesting in itself. Whomever was forced to liquidate either did not have a silver position, or else they have greater faith in that the price of the white metal will rise.

The question is: did these hapless Chinese folks sell futures or metal? And we do not have to guess the answer to this question. We have the data to show it. Read on for the only accurate picture of the supply and demand conditions in the gold and silver markets, based on the basis and cobasis.

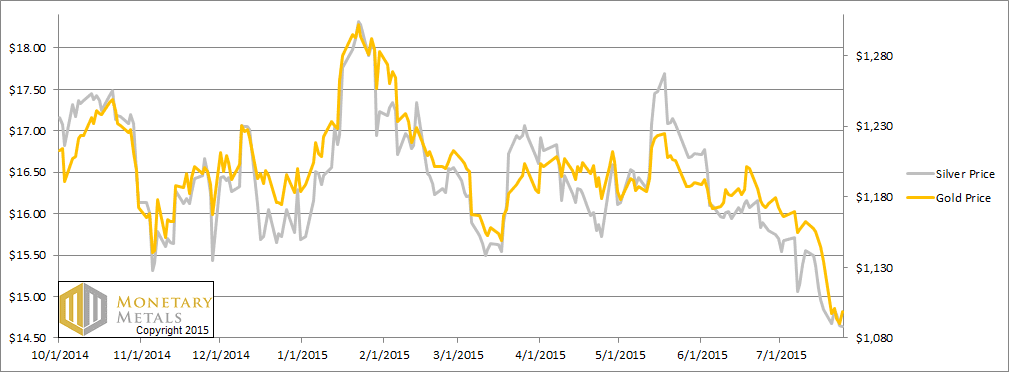

First, here is the graph of the metals’ prices.

The Prices of Gold and Silver

We are interested in the changing equilibrium created when some market participants are accumulating hoards and others are dishoarding. Of course, what makes it exciting is that speculators can (temporarily) exaggerate or fight against the trend. The speculators are often acting on rumors, technical analysis, or partial data about flows into or out of one corner of the market. That kind of information can’t tell them whether the globe, on net, is hoarding or dishoarding.

One could point out that gold does not, on net, go into or out of anything. Yes, that is true. But it can come out of hoards and into carry trades. That is what we study. The gold basis tells us about this dynamic.

Conventional techniques for analyzing supply and demand are inapplicable to gold and silver, because the monetary metals have such high inventories. In normal commodities, inventories divided by annual production (stocks to flows) can be measured in months. The world just does not keep much inventory in wheat or oil.

With gold and silver, stocks to flows is measured in decades. Every ounce of those massive stockpiles is potential supply. Everyone on the planet is potential demand. At the right price, and under the right conditions. Looking at incremental changes in mine output or electronic manufacturing is not helpful to predict the future prices of the metals. For an introduction and guide to our concepts and theory, click here.

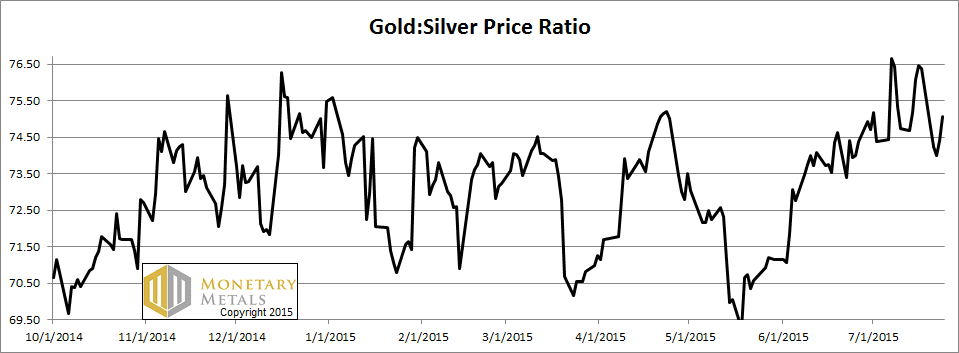

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio moved down this week.

The Ratio of the Gold Price to the Silver Price

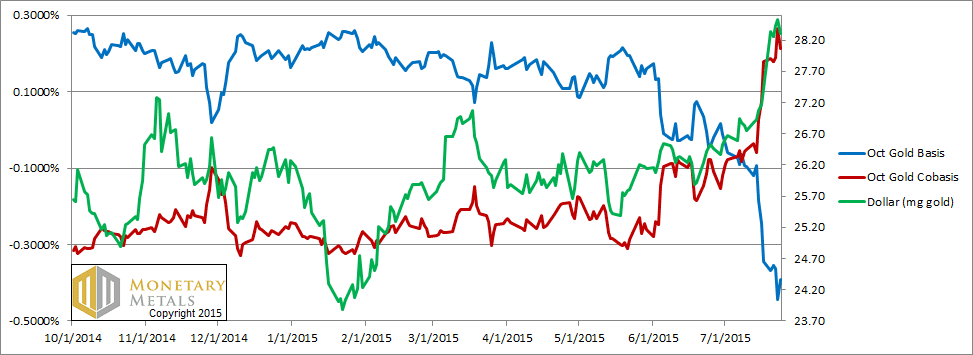

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

Note that we transitioned to the October contract, as First Notice Day for the August future approaches.

Look at the price of the dollar rising (i.e. the price of gold falling) and along with it the scarcity of gold rising. This answers the question we posed up top. The price action this week was driven by selling of futures.

Our comment last week now seems well-timed:

“Is this a good time to bet on gold? While other events could continue to dominate the fundamentals (temporarily), we can think of worse times for this trade.”

Other events—we suspect credit conditions in China—did dominate. And the attractiveness of a gold position increased this week. The fundamental price is now more than $100 over the market price. This is no guarantee that the market couldn’t go lower. The basis is not a timing indicator. It is helping us measure value.

The December contract, by the way, also entered backwardation this week.

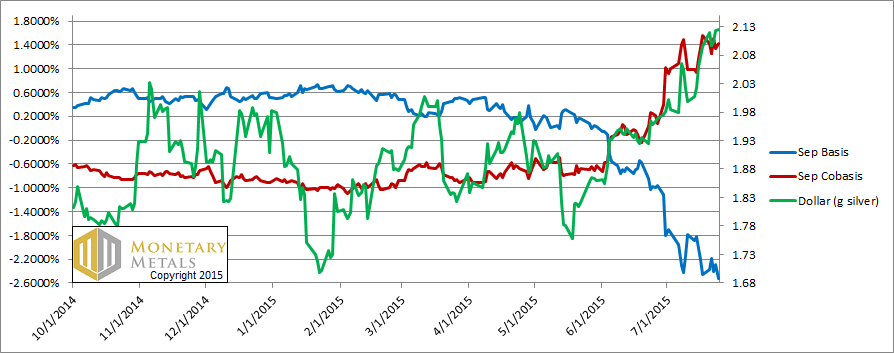

Now let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

The silver price dropped about 20 cents (i.e. the price of the dollar, measured in silver rose to about 2.12g silver). However, the cobasis actually fell. The December cobasis is nowhere near backwardation.

The bottom line is that the fundamental price of silver fell even more. It is now dead even with the market price.

We think it’s best to continue approaching silver with extreme caution. While the time is long past for shorting it (we never recommend naked shorting a monetary metal!) it is not the time for betting on silver either. We want to see either one more price drop, or else a steady increase in the scarcity of this metal to the market.

© 2015 Monetary Metals

Good one Keith!

I jut wonder if Zweig is so inundated with cartel MOPE that he really believes the crap he spews, or if he is just doing what he’s told for a paycheck, like a cheap sickly whore?

I just don’t understand why more folks don’t know that dollars are debt instruments, which is the opposite of money, and I also don’t understand why more folks aren’t doing the math. All the big banks are bust already in a mark to market reality. Real GDP is dropping, while debt keeps climbing, and we are already at the point US debt and unfunded liabilities of over $1,400,000 per taxpayer can never be made good on. FDIC insurance can only really cover less than 1 cent on the dollar. The only plausible way to prevent continuing deflation and provide liquidity to the massive $76 trillion global bond bobble is more QE. How can anyone not think US treasuries are one of the riskiest securities out there? The only reason they can continue to maintain confidence in the financial system is because folks can’t see through the facade and still have faith out of sheer ignorance! Avoid gold pet rocks at your own peril!

Agreed. This guy, Zweig is nothing but a mouthpiece for MSM. I understand the marketing of the piece, glamorous headlines that get clicks. Unfortunate that so many are attracted to this nonsense and continue to hold fiat.

As one whom has missed the greatest bull run of my lifetime while accumulating the honest, real money, Gold and $ilver, I am humored by these types of reports. Your report actually shows the balance of the fiat vs the metal, while their diatribes as singing the MOPE of the cartel and its minions.

While it is disheartening to see our physical lose value based on manipulation and over speculation, I for one would demand a much higher price than that quoted on any of the services. While not a greedy man, I do know the value.

Thank you for your reporting.

Bob: With the relentless rise in asset prices over the past 6 years, are the banks still insolvent on a mark-to-market basis? They were in 2009 when FASB let them off the hook and changed the rule. But today?

The Treasury is riskless, at least in dollar terms. The risk is only apparent when one realizes that the dollar can be abruptly repriced (i.e. in gold terms) the way the stock market was abruptly repriced in fall 2008.

Stepman: I hadn’t even thought of the clickbait angle. That’s even sadder than the standard dollar propaganda, though is it propaganda if the writer believes it?

When you say metal is losing value, what do you mean? Please don’t tell me that the price of the metal in dollars is the measure of its value! :)

First I wanted to draw your attention to the new line of pet rocks from the Royal Mint of Canada, whose backgrounds now include finely reticulated sunbursts, holograms, and anti-counterfeiting measures of true technical beauty. My apologies if this seems like advertising, I have never dealt directly with this firm, but I have to say their product takes the sting out of the coin shop premiums.

BTW, having PMs in one’s portfolio does not mean you must miss great (dollar-denominated) bull markets. I don’t know what MOPE stands for, but one of the things you hear so often that you’d think it was gold-bashing propaganda is that “stock-bearish investors should maintain a sliver (usu. 5% or less) of their portfolio in PMs”. I thought that was “panic-denial” until I did a back-of-the-envelope calculation to extrapolate their recommendation: what if the PM above ground really was 5% of global wealth? It’s Extremely stock-bearish–gold would be sold at 10-12x its price today! The “diversify” advice is right: if you’re an investor – then invest in businesses and form capital. The worst that can happen is that you’ll be able to buy more gold from weaker hands as it gets flushed out by margin calls. There is still physical out there and some of it is very pettable, if that’s what turns you on.

Jason Zweig isn’t an economist, he’s just paid to play one in the newspapers. I agree that his timing is deeply suspect in this case. As a counterbalance, I also want to link you to George Gilder’s intriguing 79 page tract on the the Entropy of money. I found it to be more incomplete than outright flawed: too breezy in spots where we know there are far better arguments. Maybe a bit too biased toward the ideas in Bitcoin, but nonetheless echoing many New Austrian core ideas!

I look forward to reading Keith’s thoughts on this, not as comment reply but in some full-review somewhere. Having real meat to chew on beats whining about Zweig’s petty insults (excuse the pun).

Gilder has been analyzing tech for decades and I’ve found him to be massively influential. I really feel the ground shifting these days. And if the battle line is drawn between the likes of Zweig and genuine thinkers, we know which side to root for; if only the history of such battles counseled just a little hope for the Good Guys…. sigh.

Wow Keith!

I see you’re on the speakers list of the Jackson Hole thing being thrown by American Principles Project. Congrats!

Can you pitch P2P digital bills as the M1 supply to front Gilder’s M0 digital gold?

If so, I will make it a priority to be there…

-g-

Greg,

I saw George Gilder talk in NY a while back, and I have read his book. I am planning to do something with it, but the world (e.g. China) keeps throwing more urgent topics my way!

I haven’t finalized my topic and theme for Jackson Hole yet, but would love to meet you there if you can make it to the conference.

Greg, MOPE is the term bandied about that means “management of perception economics”, and if I’m not mistaken, it was coined originally by Jim Sinclair. Oh, and thanks for the link to Gilders book.

I readily concede to Keith’s knowledge as to the current condition of bank balance sheets, but nonetheless we must acknowledge the G20 gave banks the legal ability to take money from depositors for a reason, and it would be remiss for folks not to realize that FDIC insurance is grossly underfunded and can’t protect them.

What exactly could be the impetus that would cause the dollar to be abruptly repriced?

I notice gold’s value is losing against organic food, which is something I care about. The history I read says gold does well in deflation (and hyperinflation, not inflation), so hopefully it will adjust!

This headline tells the story…

“Florida family finds $1mn in gold from sunken 18th century Spanish galleon”

I wonder if in 200 yrs they will say the same if somone digs up some 2015 US Dollars ?