Monetary Metals Supply and Demand Report: 29 Mar, 2015

Another week, another $18 added to the price of gold, and 20 cents to silver. We don’t generally publish technical analysis, but we keep abreast of what the technical world is saying. Not surprisingly, +$24 last week and +$18 this week have generated some excitement. In our estimation, the technicals are starting to look bullish and the price is at or near levels that indicate a breakout.

By contrast, our approach is to look at the basis. From this, we calculate a fundamental price for the metals. This fundamental price can vary from the current market price. Indeed, that’s the point. We want to know where the market price is likely to move next.

For a picture of the supply and demand fundamentals of gold and silver, read on…

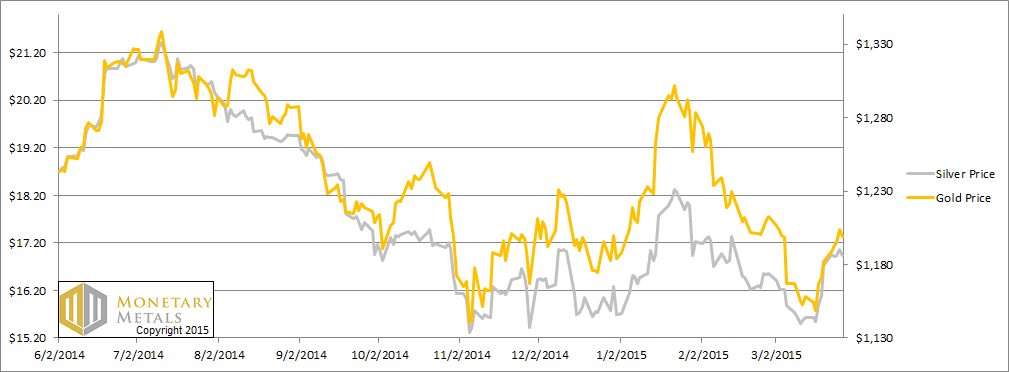

First, here is the graph of the metals’ prices.

The Prices of Gold and Silver

We are interested in the changing equilibrium created when some market participants are accumulating hoards and others are dishoarding. Of course, what makes it exciting is that speculators can (temporarily) exaggerate or fight against the trend. The speculators are often acting on rumors, technical analysis, or partial data about flows into or out of one corner of the market. That kind of information can’t tell them whether the globe, on net, is hoarding or dishoarding.

One could point out that gold does not, on net, go into or out of anything. Yes, that is true. But it can come out of hoards and into carry trades. That is what we study. The gold basis tells us about this dynamic.

Conventional techniques for analyzing supply and demand are inapplicable to gold and silver, because the monetary metals have such high inventories. In normal commodities, inventories divided by annual production (stocks to flows) can be measured in months. The world just does not keep much inventory in wheat or oil.

With gold and silver, stocks to flows is measured in decades. Every ounce of those massive stockpiles is potential supply. Everyone on the planet is potential demand. At the right price, and under the right conditions. Looking at incremental changes in mine output or electronic manufacturing is not helpful to predict the future prices of the metals. For an introduction and guide to our concepts and theory, click here.

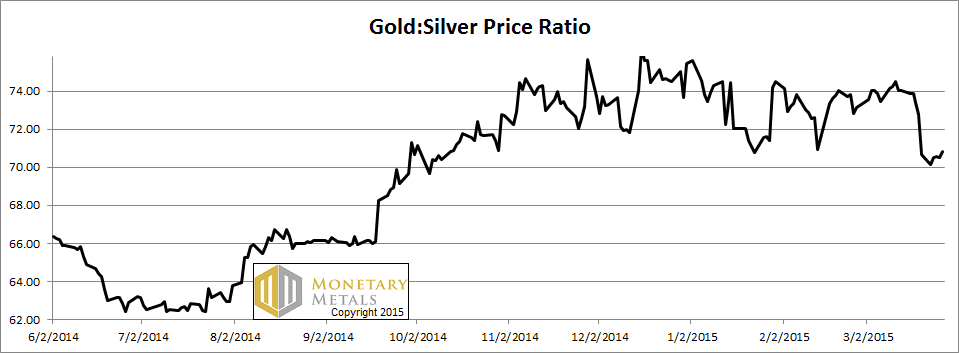

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. It moved up a hair this week.

The Ratio of the Gold Price to the Silver Price

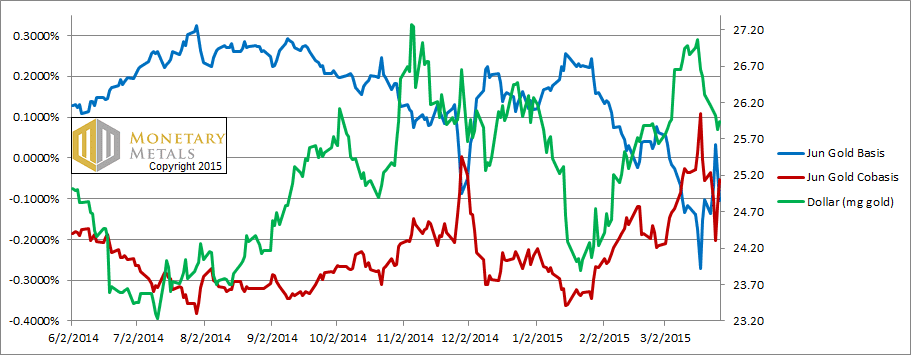

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

We shifted from the April to the June contract.

While the cobasis (i.e. scarcity) ended the week about where it began, the cobasis for farther-out months fell a bit. These past few weeks have not been big moves in the scheme of things, and with every price blip we see scarcity taken out of the market.

We would still characterize gold as a tight market, but not that tight. We calculate a fundamental price about $60 over the market.

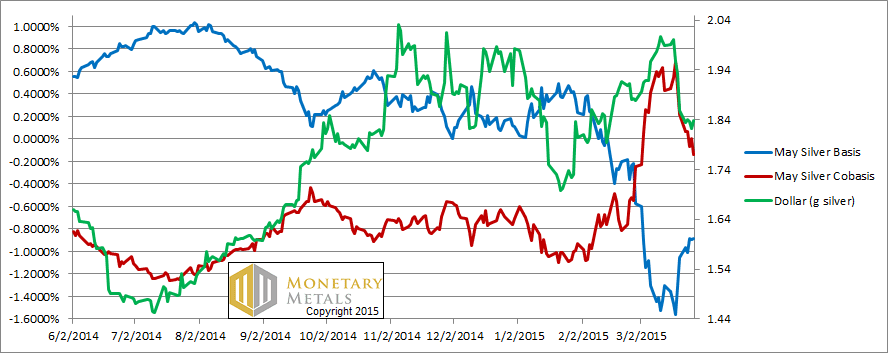

Now let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

Last week, we had backwardation in the May silver contract (though subsided from the prior week, which hit 0.6% annualized). This week, it’s gone; the cobasis is below zero. It is important to note that this is against a backdrop of soft buying of the May contract and some selling. The market knows that First Notice Day for May is approaching, and those who want to bet on silver are probably not buying May any more. Some of those holding May are starting to sell to roll to July.

With lack of buying, and some selling pressure, it is noteworthy that the price of the May contract has been rising (relative to spot). This is what it means to see rising basis and falling cobasis.

It’s an indicator.

Our calculated fundamental price dropped a bit this week, now almost a buck and a half below the market price.

To the question “what next?” we offer a different thought than we have in a long time. We think technical analysis (which, unlike the basis, is studied by most traders) is encouraging at the moment. With the caveat that silver’s weak fundamentals could suddenly matter at any time, we think it is likely that the price rises this week.

We frequently note that there is a dynamic—a system composed of multiple moving parts that interact with one another and each feeds back into the others—in the monetary metals markets. If—and this is still a big if—there is sustained buying on the technicals, it could begin to alter the fundamentals. For example, those who have been postponing their next purchase of coins could place their orders.

If rising price generates buying of metal, and not just leveraged buying of futures, we will write all about it in this Report!

In the meantime, let’s not count our eggs before they hatch.

© 2015 Monetary Metals

It’s chickens…not eggs. You’re not supposed to count your chickens before they hatch. We’re already got the egg count covered. It’s chickens we’re worried about.

Watching the basis (for me, at least) has so far been one of the best predictors of gold market behavior. Watching technical analysis has been a complete failure. I’m surprised people ascribe so much value to it.

But eggs come first…

Aren’t eggs just chicken futures by another name?

To truly answer the age old chicken, egg question requires Avery long, long, forward and back analysis. I am not ready yet to say that the MM basis, co basis is long term capable. BUT, in the short time I have been using it, I find it superb on short, weekly type prognostication. Cheers