Technical vs. Fundamental, Report 19 Mar, 2017

Every week we talk about the supply and demand fundamentals. We were surprised to see an article about us this week. The writer thought that our technical analysis cannot see what’s going on in the market. We don’t want to fight with people, we prefer to focus on ideas. So let’s compare and contrast ordinary technical analysis with what Monetary Metals does.

Technical analysis, in all of its forms, uses the past price movements to predict the future price movements. In some cases (e.g. momentum analysis) it calculates an intermediate signal from the price signal (momentum is the first derivative of price). But no matter the style, one analyzes price history to guess the next price move.

This is necessarily probabilistic. There is no way to know that a particular price move will follow the chart pattern you see on the screen. There is no certainty. And when it does work, it is often because of self-fulfilling expectations. Since all traders have access to the same charts, and the same chart-reading theories, they can buy or sell en masse when the chart signals them to do so.

We are not here to argue for or against technical analysis. We simply want to say that it’s not what we are doing. Not at all.

Our analysis is based on different ideas. The key idea is that there is a connection between the spot and futures market. That connection is arbitrage. Think of each market as a platform that moves up and down on its own vertical track. The two tracks are close together. And the platforms are connected to each other by a spring. Suppose platform A is a bit above platform B. If you push up on A, then the spring stretches a bit more and will pull B up, though perhaps not as much. The same happens if you push down on B.

Conversely, if you push down on A, then it will compress the spring and platform B will tend to go down, though not as much.

A and B are the futures and spot markets for gold (the same analogy applies to silver). Arbitrage works just like a spring. If the price in the futures market is greater than the price in the spot market, then there is a profit to carry gold—to buy metal in the spot market and sell a futures contract. If the price of spot is higher, then the profit is to be made by decarrying—to sell metal and buy a future.

There are two keys to understanding this. One, when leveraged speculators push up the price of gold futures contracts, then that increases the basis spread. A greater basis is a greater incentive to the arbitrageur to take the trade. Two, when the arbitrageur buys spot and sells a future, the very act of putting on this trade compresses the spread.

If someone were to come along and sell enough futures contracts to push down the price of gold by $50 or $150 or whatever amount is alleged, then this selling would be on futures only. It would push the price of futures below the price of spot, a condition called backwardation.

Backwardation just has not happened at the times when the stories of the big “smash downs” have claimed. Monetary Metals has published intraday basis charts during these events many times.

The above does not describe technical analysis. It describes physics—how the market functions at a mechanical level.

There are other ways to check this. If there was a large naked short position in a contract that was headed into expiry, how would the basis behave? The arbitrage theory predicts the opposite basis move. We will leave the answer out as an exercise for the interested reader, as thinking this through is really good work to understand the dynamics of the gold and silver markets (and you can Google our past articles, where we discuss it).

This check can be observed every month, as either gold or silver has a contract expiring (right now it’s gold, as the April contract is close to First Notice Day).

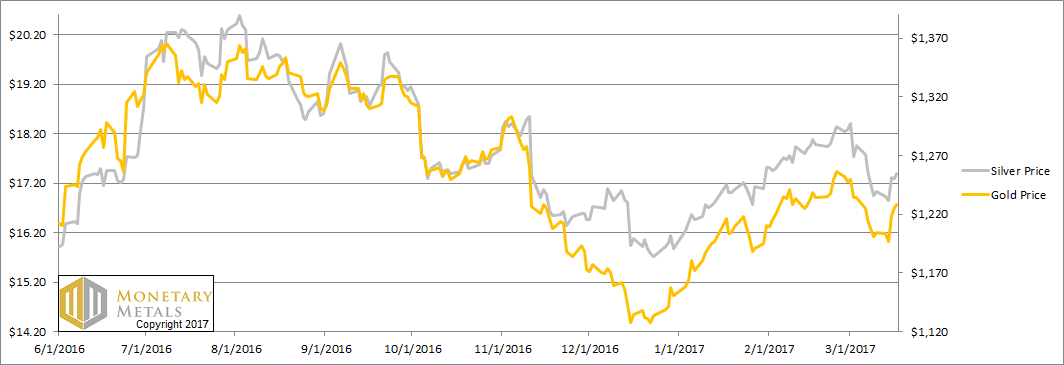

This week, the prices of the metals both rose. The price of gold is almost back to where it was the prior week, but that of silver is not.

Below, we will show the only true picture of the gold and silver supply and demand. But first, the price and ratio charts.

The Prices of Gold and Silver

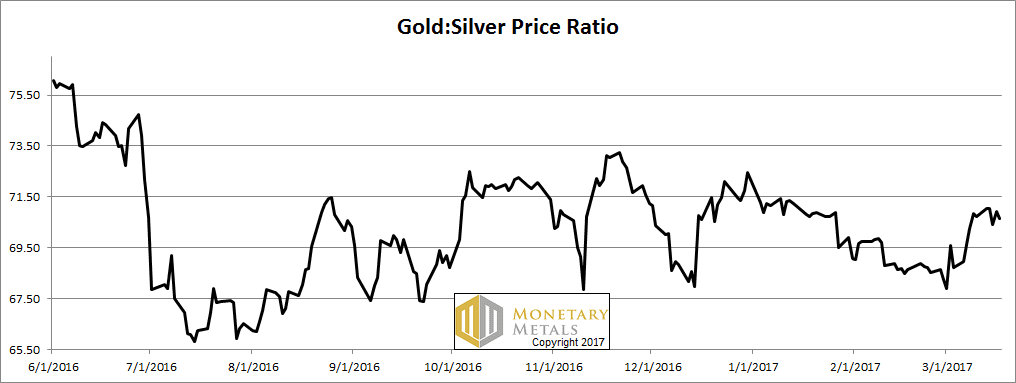

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. It moved sideways this week.

The Ratio of the Gold Price to the Silver Price

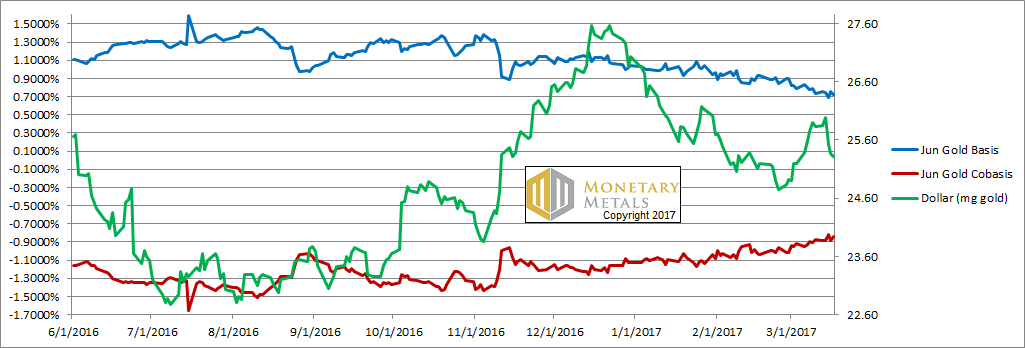

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

NB: we switched from the April to the June gold contract.

As the price of the dollar fell (inverse of the rising price of gold, measured in dollars) we see the cobasis (our measure of scarcity) increased a bit. This means the buying in gold, which pushed up the price, was buying more of physical than of futures. This seems to be the new pattern of late, though it is sputtering a bit like an engine trying to start up and run at a steady RPM.

Our calculated fundamental price of gold is up nearly $50. It is now over $1,400.

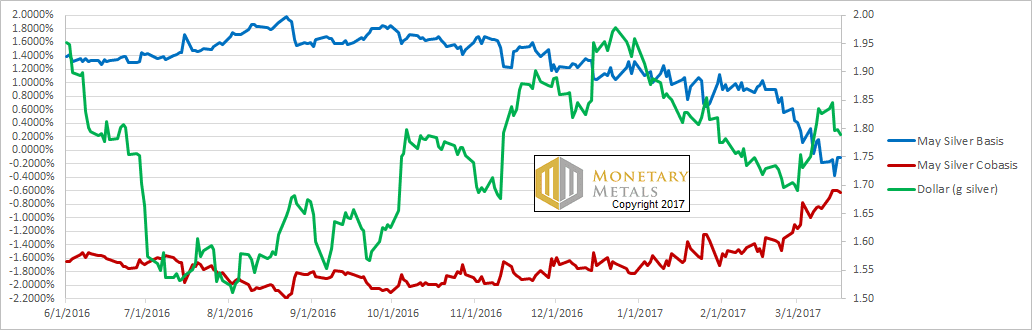

Now let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

The story is the same in silver. Rising price accompanied by rising scarcity.

The silver fundamental price rose 50 cents. It is now aboit $1.30 over market.

Make sure to subscribe to our YouTube Channel to check out all our Media Appearances, Podcast Episodes and more!

Additional Resources for Earning Interest on Gold

If you’d like to learn more about how to earn interest on gold with Monetary Metals, check out the following resources:

In this paper we look at how conventional gold holdings stack up to Monetary Metals Investments, which offer a Yield on Gold, Paid in Gold®. We compare retail coins, vault storage, the popular ETF – GLD, and mining stocks against Monetary Metals’ True Gold Leases.

The Case for Gold Yield in Investment Portfolios

Adding gold to a diversified portfolio of assets reduces volatility and increases returns. But how much and what about the ongoing costs? What changes when gold pays a yield? This paper answers those questions using data going back to 1972.

OK, so $170 over $1,230 thus the futures price “SHOULD” be pulled up. We shall see.

Perhaps another way to look at the market: Why isn’t the price of gold much lower? Stocks at new highs, high confidence in the economy and banking system, bank stock rising, WHAT’S to worry. I thought gold would be sub-$1,000 by now–WTF?

Somethin’ strange afoot.

“$170 over $1,230 thus the futures price “SHOULD” be pulled up” – No.

Keith’s calculated fundamental price can change in next week’s report. Think of it as a weather report. It’s not backward-looking; but really, it’s not all that forward-looking either. The weather always changes. Predicted future weather often doesn’t come true, because it’s a chaotic system. Markets are chaotic because people have choice. Any of the participants can change their behavior by next week, creating new market forces and directions (if enough of them do it).

What value does Keith’s calculated fundamental price have? The one thing it tells you is whether speculators have made gold relatively cheap for you, RIGHT NOW. Keith is saying that, IF the influence of speculators could be removed, today’s price would be up at $1400. Thus, actual market at $1230 is a good deal for buyers. The theory (which I personally have NOT seen tested/proven) is that, if you always buy when Keith’s fundamental price is above market and sell when it’s below market, then you’re beating the speculators at their own game and (over time) generating a profit.

What I don’t get is, how the fundamental price can be so far above market when the basis is still pretty high. In the June graph, we see a basis of +0.7%; declining (due to increased physical buying), but still substantial. It implies that speculators still own a lot of futures / are net long, which gives the warehouseman his incentive to carry. But a fundamental price of $170 over market implies that speculators have sold many of their futures into the market / are even possibly net short. I don’t see how both things can be true at the same time. Keith or Bron, could you explain?

I could be wrong about this, but my understanding is that the fundamental price takes into account prevailing interest rates and storage costs.

So 0.7% is actually very low considering that the Federal Funds Rate is at 0.75-1.00%.

To compare apples to apples, the 3-month basis in July was 2% while the FFR was 0.25%-0.5%. That means the basis was 1.5%-1.75% above the FFR.

That’s very high. And at that time, Keith was saying that gold was trading at a premium over its fundamental price.

But now the 3-month basis is 0.7% and the FFR is 0.75%-1%. So the basis is 0.05%-0.30% BELOW the FFR.

So a swap dealer who sells futures is actually taking a loss right now if he borrows money to buy his spot gold…or he’s missing out on a gain if he pays cash for the spot gold.

As a result, in theory there are not many people doing swap deals for gold right now. So there’s not enough people holding gold to be delivered in the future. Which means there’s a chronic shortage.

I’m not implying that Keith actually uses the FFR is his “fundamental price” calculation. But I’m pretty sure he says in one of his articles that he uses an “interest rate” in his calculation.

So it could be LIBOR or Treasury bond rates or something else.

But that could explain the paradox you are describing.

Good suggestion: the warehouseman has an opportunity cost, which is something like LIBOR / FFR. As those rise, 0.7% basis could seem low.

But if that’s true: it would seem to imply that historically interest rates like 5-10% will see a similarly high gold basis. Does anyone know if that’s true?

From what I’ve heard, the basis was high in the 1980’s and 1990’s. It was close to 10% in the early 80’s. Seems shocking now, but it’s apparently true.

There’s an essay by Tom Szabo called “Gold and Silver ‘Leasing’ Examined” that goes through the whole history of how the bullion banking system evolved. It explains a lot of this stuff…including the correlation of the basis with interest rates.

Actually, he doesn’t specifically call it “the basis”. He calls it “the GOFO rate” or just “GOFO”. But it’s basically the same thing. GOFO is the “basis” for the OTC market, whereas what Keith is providing us with is the “basis” for Comex. But Szabo mentions in his article that the Comex basis and the OTC GOFO rate are always very close to each other. So it’s pretty much the same thing.

But yeah, according to him and a few other people I’ve read…the basis was much higher in the 80’s and 90’s.

Unfortunately, I don’t remember where I found the Szabo article except that it was a dead link and I had to find an earlier version of the page on archive.org.

But it’s a fascinating article if you can ever find it and get the chance to read it.

Yes you are right, the cost of “money” is an input into the calculations of an arbitraguer and thus into Keith’s fundamental price calculation.

Thanks Bron.

Note this from Mish below and the fact that Switzerland is currently pulling in gold at an annualized very high rate in 2017 (a record rate in fact although it’s early days obviously). Formerly gold was net-exported from Switzerland in years 2013-16.

This gold is partly being pulled in from HK and UK while significant flow from UAE to Switzerland is continuing at a historically high rate since early 2016.

Meanwhile we will likely see significant year-on-year improvements of Indian demand in the months ahead, particularly Swiss to India flow, the main supply channel.

https://mishtalk.com/2017/03/20/non-euro-investors-dump-e192-billion-bonds/

Yes it seems to have switched around in the first few months of this year. Nick Laird’s charts are showing net flow of 15t a month from UAE since Oct 2016, but that is down from average of 40t a month during Feb-Sep 2016. UK has a clear shift, hopefully Nick doesn’t mind me sneaking in this chart

ISTANBUL, April 4 (Reuters) – Turkish gold imports rose 17-fold to 28.2 tonnes in March, as Turks looking to hedge currency risk ahead of a referendum in two weeks time followed President Tayyip Erdogan’s calls to buy gold instead of dollars.

After the sharpest falls in the Turkish lira since the 2008 financial crisis last November, Erdogan called on Turks to sell dollars and buy lira or gold to prop up the local currency. Gold imports have been rising year-on-year ever since. “People have started opting for gold rather than foreign currencies,” said Mehmet Ali Yildirimturk, a gold specialist in Istanbul’s Grand Bazaar, adding that a moderate recovery in the lira had also made gold more affordable again.

http://www.kitco.com/news/2017-04-04/RPT-Gold-imports-surge-as-Turks-heed-Erdogan-apos-s-call-and-vote-looms.html

And at the same time “Turkey to give central bank first option on buying domestic gold” (http://www.reuters.com/article/turkey-cenbank-gold-idUSL5N1H53VN) and “Turkey to introduce sovereign gold bonds, gold lease certificates” (https://www.dailysabah.com/economy/2017/04/03/turkey-to-introduce-sovereign-gold-bonds-gold-lease-certificates) although the latter aren’t real gold bonds given the yield is paid in lira.

Tom Szabo did write some good articles, they were on his http://www.metalaugmentor.com website which is closed now. You may have luck searching on http://web.archive.org/web/*/metalaugmentor.com for pages pre 2014.

Regarding GOFO, arbitrage again forces a connection between OTC forward rates (of which GOFO was only an indicator) and futures market basis figures. We will have something exciting on that front to announce shortly.

Couldn’t find the Szabo article. If anyone can find it, please post the link.

Update – The fundamental price of $170 over market is indeed much too high, as Keith reveals here: https://monetary-metals.com/mea-culpa-report-9-april-2017/

Your blog has quickly become my go to place come Monday mornings. It is interesting to see the steady ascent of the co-basis week after week and having an indicator that is looking forward and not looking back.

However recent news items don’t thyme with this co-basis trend. First we have this ZeroHedge article claiming that demand for physical bullion is plunging (http://www.zerohedge.com/news/2017-03-17/demand-physical-gold-collapsing). Then I today got an email from BullionStar announcing the lowest ever premium on silver coins. Finally I understand that global jewelry demand is way down 2016 (https://www.bullionvault.com/gold-news/gold-demand-012720173).

These news items do not confirm tighter final demand. So how can the rising co-basis be explained? Might it be that paper gold takes up the slack or might it reflect demand for other forms of gold like 400 oz Good Delivery Bars, or are there entirely different forces at play here?

Ponast, the Simon Black article at ZeroHedge is “fake news”. It’s a shame that Zerohedge published it…because I normally like their articles.

Demand for gold in monetary form (retail coins and bars, ETF inflows, exchange and bullion bank inventory builds, central bank purchases) increased by 635.9 tonnes in 2016. Part of this gold was made available because of an increase in mining output of 73.2 tonnes. Another 563 tonnes came from a reduction in jewelry, technology and dental demand. 0.3 tonnes are unaccounted for.

This is all in the data supplied by the World Gold Council’s “Demand Trends Report”.

When the price of gold goes up, jewelry/technology/dental demand goes down. When the price of gold goes down, jewelry/technology/dental demand goes up. This is just the way the gold market works.

Regardless, there’s definitely not been a fall in demand for retail bars and coins. It went up by 10.9 tonnes. That’s not a lot. But it’s still an increase.

So basically, the ZeroHedge article is nonsense.

Yes, conventional analysts have been discredited for some years now. Thanks, Keith.

Gold futures market trades around 90:1 versus the approximate 4 tonnes of metal gold and derivatives multiple hundreds more daily, This might explain the scarcity against rising prices that Kieth has mentioned since December 16. The fake market is showing signs of stress which will possibly end in a reset as mentioned by Andrew Maguire recently.

Unlike most commodities which are consumed Gold is one market where there is no need for futures because supply is known production is known, supply and consumption are relatively stable, real time and real metal delivery should be the only price setting mechanism for Gold I suspect the market will change soon.

I found the Szabo article in question here:

http://web.archive.org/web/20101214124449/http://www.silveraxis.com/commentary/gold_silver_leasing.pdf

Not a bad read.

I would note that what he calls “GOFO” is the more simplistic Spot Price – Future Price.

The Monetary Metals stuff here refines things further as:

Basis: Future (bid price) minus Spot (ask price)

Cobasis: Spot (bid price) minus Future (ask price)

Both can potentially be negative, at most one can be positive.

So, the silver basis just dropped below zero in the above chart. Is silver now in backwardation? Or do we have to wait for the cobasis to rise above zero as well? I’ll stop at 2 questions. Slowly making sense of this.Thanks!

Yes really you need cobasis positive, ie a profit can be earned from selling spot and buying futures, before you have backwardation. However I think just because the cobasis pops its head above zero and you have technical backwardation, you really need that to be a lot more positive and across other contracts, not just near, before it a real market signal. Or another way of putting it is http://goldchat.blogspot.com.au/2013/07/shortodile-golddee-thats-not.html

Perfect, and thanks for the crocodile Dundee analogy! Lol.