Part I

Last Thursday, January 28, there was a flash crash on the price chart for silver. Here is a graph of the price action.

The Price of Silver, Jan 28 (All times GMT)

If you read more about it, you will see that there was an irregularity around the silver fix. At the time, the spot price was around $14.40. The fix was set at $13.58. This is a major deviation.

Many silver bugs are up in arms about how unfair the new silver fix is. That’s nothing new. They were up in arms about the old one. The old one was supposedly manipulated.

One thing is for sure, tactical manipulations can occur. A gold trader in London was found to have pushed the price down in the gold fixing by a few pennies. He had sold a multimillion dollar option, and he wanted it to expire worthless to avoid having to pay. Right after the fix, he bought back the gold he sold, pushing the price back up to where it was. He took a loss on the round trip of the gold, of course, but saved millions on the option which he did not have to pay.

This is not the long-sought proof that nefarious forces are keeping gold from attaining $20,000.

Anyways, because the silver and gold fixes were deemed to be benchmarks by regulatory changes post the LIBOR manipulations, a new process for the gold and silver fixes was implemented. Before we look at what changed, let’s consider why there is a fix price. Couldn’t they just take the price at 12:00 noon?

No, it wouldn’t work because in a live market there is not just one price. There are always two prices: bid and offer. Which would you use as the benchmark? Either price could misrepresent the current state of the market. What’s more, those prices are just quotes, not executed trades.

To be useful as a benchmark—a price that third party contracts and derivatives can be based on—there has to be a single price based on real executed trades. So they need to get buyers and sellers together, and find the price at which the most metal clears. If there is a better way than that, it hasn’t been discovered yet.

This leads to a question. How do two prices that are supposed to track each other actually, you know, stay matched? This occurs in Exchange Traded Funds that move with an index of stocks (such as SPX or GLD). It occurs in gold futures and spot.

It should also occur between the fixing process and the spot market. What use is a silver fix at $13.58 while the spot price was $14.40? We’ll get back to market action on that day, in a bit. First, we need to look at the force that keeps two prices close to each other.

It is arbitrage. Let’s use GLD as an example. Each share represents a known quantity of gold. Suppose the price of the share rises relative to the price of gold metal in the spot market, and the metal in a share of GLD is $1 per ounce higher. The arbitrageur buys gold metal, creates shares of GLD, and sells them. This tends to pull up the price of gold metal, and mostly pushes down the price of GLD.

Note that the arbitrageur takes no price risk. He is simply acting to profit from a spread (usually a very small one). Arbitrageurs will keep doing this trade, until GLD and gold metal get close enough that the small remaining profit is not worth the effort.

The arbitrageur is motivated, of course, by profit. He is as greedy as the next guy (admit it, if you could demand a 300% raise from your boss, you would). However, his activity is self-limiting. The more he puts on his trade, the more he compresses the spread. In our example, the arbitrageur buys some gold metal and sells some GLD shares, to make $1. That is the initial profit. However, he compresses that spread, perhaps to 50 cents. He can have another go, but then the spread narrows to 25 cents. Soon enough, he walks away (these are illustrative numbers only for this example).

It’s a textbook case of the Invisible Hand described by Adam Smith. The arbitrageur, seeking his own profit, ends up serving other market participants. He keeps two different prices locked tightly together. Everyone else can take for granted that GLD works as it’s supposed to.

For example, suppose you run a small gold coin store. You need to hedge your inventory just as a large dealer does. However, you sell gold one ounce at a time. Big dealers might use 100-ounce gold futures, but you use GLD. You can thank the actions of this arbitrageur.

Now let’s get back to the fix. The old process was conducted by the major market makers in each metal. They got together in one room, and each had major clients on various phone lines. The chairman would put out a price, and the market makers would talk to their clients to determine who wanted to sell at that price and who wanted to buy. Then they add up all selling and buying, and see if there’s a close match. They would keep moving the price until selling matched buying within tolerance. That was the fix price.

There was just one problem, at least so far as the gold bugs were concerned: the market maker. Since the first market maker walked into a coffee house in London where shares were being traded, most people have misunderstood the market maker. Back in the coffee house days, all potential sellers would line up on one side of the room, in order from lowest offer price to highest. On the other side, buyers would line up, from highest bid to lowest.

If one had to sell, that meant taking the best bid presented in the room. Likewise, if one wanted to buy right now, one paid the best offer price. As you would imagine, the bid-ask spread could get pretty wide, and perhaps worse yet, it was unpredictable.

Until the market maker walked in. Unlike all the others, he was both a potential buyer and a potential seller. He had an inventory of both shares and cash. He published a better price if you wanted to buy or sell and as it turns out, he was the only one who could consistently buy at the bid price and sell at the ask price.

Of course, the guy with the best bid price—or what had been the best price until the market maker strolled into the room—was upset. Who is this dodgy bloke? Why is he allowed to mess about like this? Surely it’s unethical, immoral, and maybe even illegal?

In fact, he is serving all market participants (except the few who hoped to sell and make a buyer pay a premium and the equally small few who hoped to buy from someone desperate to raise cash). The market maker is motivated by profit, sure, but in making money he is narrowing the bid-ask spread whilst also reducing its volatility.

Today, the market maker is aka High Frequency Trader, and he uses technology that the coffee house fellows could not have imagined. Nevertheless, he too encounters the same exact suspicion, if not resentment, if not envy and anger.

Now let’s tie this to the silver fix. In the old fixing process, bullion bank dealers could place orders in the spot market during the fix. For example, if the fix price looked like it might settle at $14.30, but the spot price was $14.34, the dealers would buy the fix and sell spot, happy to make four cents.

Many objected to this because it looked like information was leaking into the market. They claimed it’s so unfair, perhaps even a gateway drug to insider trading? If other market participants can’t have this privilege, the bullion banks shouldn’t have it either. And besides, they’re supposed to be just brokers and not trading their own proprietary positions. The truth was that there was nothing stopping other market participants from also trading in the spot market during the fixing process, it was just that the bullion banks’ dealers were more efficient at being market maker.

Well, in part due to the agitation of the gold and silver bugs, government regulators came down on the market makers. They fixed it so that market makers were no longer allowed to arbitrage the fix to the spot and futures markets.

Before you think “yeah, this is what we want,” let’s revisit one of our favorite and recurrent themes, namely: be careful what you wish for.

As it stands today, if the fix price is starting to deviate from the market price, the market makers’ hands are tied. Ross Norman, CEO of bullion dealer Sharps Pixley in London, expressed his frustration with this. “The real problem as we see it is that banks are increasingly unwilling or unable to place corresponding orders where they perceive a mis-pricing because of fears of being accused of abusing a situation and facing the wrath of the regulator or their compliance departments.”

The big clients who participate in the fixing process may be freer to trade. However, they don’t have the same information. Market making is hard because you’re playing for pennies or fractions of a penny, but if you screw up you can lose dollars. The clients may know how many rounds into the fixing process they are, and the order imbalance of each round. But they can’t react as quickly as the bullion banks who are making markets in the spot, futures, and ETF markets, and they don’t know as much about market conditions either. They can’t arbitrage a few pennies. They need a much bigger spread.

A wider spread, much less an unpredictable spread, is to no one’s benefit. For example, the mining companies often sell at the fix price, rather than try to time it (or be accused of breach of fiduciary duty by their shareholders if they mis-time it). How much deviation of the fix price will it take before miners are forced to embrace the next-best solution?

“The large discrepancy between the spot price and the fix is very alarming to us especially that it happened twice in a row,” KGHM head of market risk Grzegorz Laskowski told FastMarkets.

The next best solution, by definition, is less advantageous than the best.

Part II

The first thing worth noting is the timing of the move in the public silver markets. It occurred at 12:15pm GMT. The London Bullion Market Association says, “The [silver] price is set daily in US dollars per ounce at 12:00 noon London…” The market went bananas because the fix price was more than 80 cents cheaper than the market price. What was the cause to drive the market?

Someone bought silver at the fix. They bought enough to finally (more on this is a moment) balance the sell orders. If the banks aren’t allowed, then the price has to go down far enough that other market participants find it worthwhile to take the price. They are taking a risk that the market price will be high enough that they will make money, or at least not lose it.

As this screenshot of the silver fix shows, it took 29 rounds at 30 seconds a round which is why the process did not finish until 12:15.

Source: https://www.bullionstar.com/blogs/ronan-manly/lbma-silver-price-scandal/

Note the buy (bid) and sell (ask) volumes, the auction gets “stuck” by round 9 where the amount people were willing to buy was not increasing from 27, whereas the sell volume was 34 lots (1 lot = 100,000oz). The algorithm that sets the price for the next round therefore keeps on dropping the price to draw out more buyers but you can see there is no response – the bid volume is stuck at 27 lots. With each price drop the volume offered for sale increases, presumably as stop losses were triggered. So it wasn’t a case of selling pushing down the price (34 lots = 3,400,000oz, which is only 680 Comex contracts) but a lack of buyers. Only when the price reaches $13.60 in round 28 do we see an additional 27 lots of buying appear with the fix set in the next round.

So what happened at that time? Anyone who bought silver at the fix price–$13.58—wants to close the other leg of their arbitrage. They need to sell. They have a choice of what to sell. Not counting SLV (the NYSE was not open at this time anyway), they can sell either futures or spot.

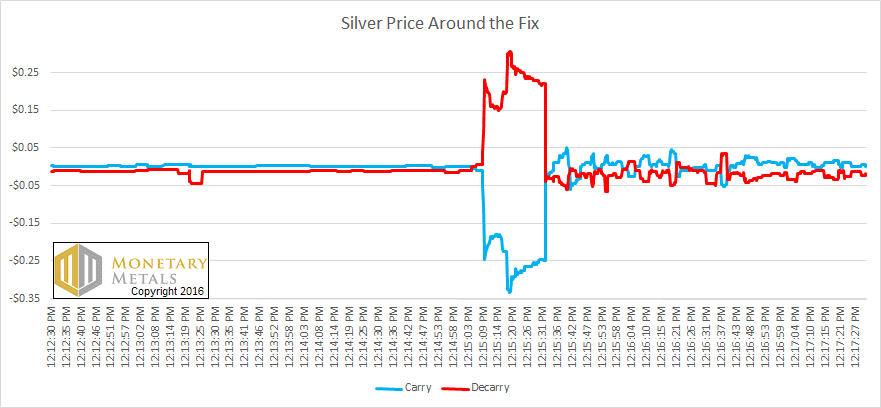

Wouldn’t it be interesting if we could tell which they sold? We can glean that from a chart of the silver carry.

March Silver Carry and Decarry

This graph shows the raw carry and decarry (in dollars), as opposed to our normal format of basis and cobasis (in annualized percentages). We are looking at only a few minutes, so annualized percentage is not adding anything. More importantly, it is interesting to see the magnitude of the arbitrage profits and how it changes.

To review, carry is the profit you make to buy spot and sell a future. It is the profit offered to the warehouseman, who stores a good for delivery to a futures buyer at maturity of the contract. No one will perform this service without a profit. Decarry is the profit to unwind a carry position, that is sell spot and buy a future. Sometimes the warehouseman is offered this incentive (in conditions of scarcity).

Back to the graph. We can see that no information “leaked” into the market, before the fix was complete. This accords with the fix rounds, as it was only in the last minute that a buyer(s) stepped in with volume. The carry holds steady at around $0.002 per ounce. We are not in the market making business, but we’re pretty confident to say that no one will take this arb—that is, carry silver—for a mere 2 tenths of a cent. The decarry is negative, so definitely no actionable trade there.

Then, *BOOM*.

Suddenly, at 12:15:05 the decarry goes positive. At first, it’s only $0.001. However, within four seconds, it goes to $0.04. Then in a split second to 9 cents, and then 23 cents. A 23-cent profit to decarry silver?! That’s about 1.7%, not annualized (which would be a big profit on a risk-free trade in The Fed’s zero-interest rate world) but 1.7% on a March contract. This is nearly 10% annualized.

What is going on here?

The traders who bought silver at $13.58 in the fix are unloading, to lock in their profit. They have the metal (likely purchased with borrowed funds) and need to unload it to make dollars. They have a choice between selling it in the spot market, or selling futures contracts against their metal.

Decarry = Spot – Future. So if decarry is rising, then it’s either a rising bid on spot (which we know was not the case from the price action) or a falling futures price.

Those who bought silver metal at the fix unloaded it, by selling futures. This describes how it’s supposed to work, and how it has always worked. The difference is that those in the position to do this with the least risk, and therefore at the least cost, are barred from doing it. Others have to take on this job. Since they incur much higher risks, they charge a lot more. And the aftermath is very ugly, as we saw on January 28.

After the fix information hit the public markets with an initial bang, volatility continued for a long time. One can imagine that stop orders were triggered, then limit orders filled, and so on, as technical traders, price-sensitive buyers, overleveraged speculators, and others were perturbed. No one is served by this, except a few nimble traders.

One group who most definitely does not benefit from this is the silver mining companies. They are price takers. If you are invested in silver miners, then you have a vested interest in seeing a robust process for setting the benchmark price of silver. Even if you just speculate on the metal, and want to see the price of silver rise, you should support a fix process that allows the market makers to do their job. A broken benchmark and wicked volatility does not inspire confidence for most people who might consider buying silver.

© 2016 Monetary Metals

“Suppose the price of the share rises relative to the price of gold metal in the spot market, and the metal in a share of GLD is $1 per ounce higher.”

… You meant to say the share is $1 per ounce higher than the spot metal — assuming the spreads are well less than $1.

Compelling and informative reading. Thank you.

Thanks Keith for an excellent explanation.

Cheers

Why would they want to inspire confidence in their antithesis ?

With basically 24 hr trading nowadays,just exactly what is the point of a Fix anyway?

Should not the market be open and fluid at least for a whole trading week?

Stocks settle at COT and we are just left with an bid and ask on Monday morning.

Thx Steve

Thanks for your comments.

Many companies, big and small, need a reference price for their business. Mining companies are one. I advise a small company who is using the fix price in its dealings with its customers. A live bid-ask pair does not serve this need. Or not as well. If the fix no longer works, everyone will make do.

There are many other examples of the tragedy of making do: homeschooling, barter networks, chopping your own firewood, diagnosing and treating your own medical conditions… most of them (with a few exceptions) are due to the government preventing people from coordinating their activities in the economy. Impoverishing the people… a whole separate theme.

Thanks Keith, that is very enlightening. And the “tragedy of making do” – what a profound and accurate turn of phrase.

Hi Keith ;

I have a simple question, why do we need a fix in Gold and Silver ?

Why cant Gold and Silver be sold just like a stock price in a stock-exchange and everybody can see it ?

This will eliminate any questions about the price since it will be visible to everybody.

Gold and silver futures are sold in an exchange, Gold metal is sold with prices anyone can see (though the market is not a standardized exchange). The issue is that many parties around the world need a referenceable price. “On Feb 9, gold was $1191 (PM)”. That is the fix price.

I fully agree with Dave H !

Hi Keith,

Between rounds 9 and 27 when the bid volume was ‘stuck’ at 27 lakhs, the ask volume was still increasing incrementally and quite uniformly over each round, and in a lot of cases, going up by 1 lakh per round. I find this pattern hard to align with just stop loss orders since it doesn’t look random. Its also odd (to me) that there were no buyers coming in whatsoever when the price was falling between rounds 9 and 27. This begs the question, which physical silver user clients are even participating in the auction as clients of the direct participants, that no one even amended an order.

manly: it’s hard to know what they may have been thinking. But one thing’s for sure. Arbitrage was out. The banks couldn’t buy the fix and sell spot or futures. To everyone else, they’d have to be wondering what the reason is, they’d have to see the falling fix price with each round–2 cents and a few rounds later the increment would change to 3 cents.

The bidders come in when the price has well and truly broken down–and parties who aren’t normally market makers could finally be comfortable that buying at the fix would not just be catching a falling knife.

Bonjour Keith,

After 28 years as a Stock-Broker and 10 years as an Author an Consultant, I have read

multitudes pieces of information, but Thank you, yours is so simple and straight forward.

Keep the good work.

Best regards,

Yvon Sheridan

MONTREAL