Temporary Backwardation: The Path Forward from 2008

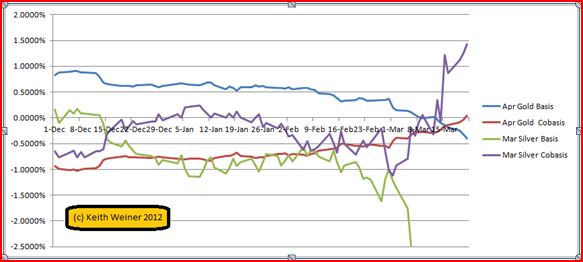

The March silver futures contract first entered backwardation on Mar 9 and with a few zigs and zags has not only remained there but has gone deeper and deeper in. The April gold future just entered backwardation today. See the graph (backwardation is when (Spot(bid) – Future(offer) > 0).

We shall see what the coming days bring for the April gold future, but the fact that backwardation has occurred at all is significant. The fact that it is now a “normal” occurrence since fall 2008 indicates a deep pathology.

I have written in the past about gold and silver backwardation (Debunking Gold Manipulation, Decline and Fall of Silver Backwardation, Is Gold Backwardation Now Permanent). The gist is that one can look at the spread between the price of a future vs. the price in the spot market of the same commodity.

We define the basis as the Future(bid) – Spot(ask) and the cobasis is, as mentioned above, Spot(bid) – Future(offer). In a normal world, the basis is positive and it is basically given by the rate of interest. The cobasis should be negative unless there is a shortage. A shortage of gold or silver is meaningless as people have accumulated enormous inventories of the stuff over thousands of years.

But in the “new normal”, post 2008, the expiring gold or silver future often flirts with or even slips into backwardation for a period before expiry. This is anything but normal. It’s not a sign of imminent financial Armageddon, but it is a sign that beneath the surface there is a growing rot in the core of the system. Why?

The short answer is that no actionable opportunity to make free money should last more than a millisecond (or less, due to High Frequency Trading). If one can see a “risk free profit” sitting on the screen day after day, let alone if this profit is growing, this is a sign that All Is Not Well even if one doesn’t know why or what specifically is happening. Backwardation means that anyone who has gold or silver could simultaneously sell the metal and buy futures contracts to recover their position, and make a profit. And, given the enormous stocks of gold and silver, many people have lots of gold and silver.

The backwardations that are “normal” today are too small for the retail trader to profit from, given that he must pay commissions. But they are easily large enough for many institutions that make a market in gold (especially compared to their alternatives for short-term capital). The following question remains unanswered:

Why do institutions not take the risk-free profit offered to them in gold and silver?

I don’t believe it’s because they are afraid of the risk. I make this statement in light of two facts: (1) the near-month future expires very soon (about 5 weeks for April gold or a week for March silver) and (2) the farther-out futures are not in backwardation. The financial system is not going to collapse in 5 weeks, and if it were then the farther futures would fall further into backwardation. Trust in delivery 5 months from now would be less than trust in delivery 5 weeks or 5 days from now.

As a reminder, to profit from contango, one must buy physical and sell a future against it to end with the same net position plus a small profit. To profit from contango, one carries the metal. Think of carrying as like warehousing it for a small fee. The only prerequisite is that one needs cash (or more typically credit). Carrying will push up the ask in physical and push down the bid in the future, thus reducing the basis.

In contrast, to profit from backwardation, one decarries by selling physical and buying a future. The prerequisite is that one needs the metal. One could either sell one’s own metal, or if one had previously carried metal one could unwind the carry. Either way, this would push down on the spot bid and up on the future ask until the cobasis was zero or negative.

For whatever reason(s), this is either not occurring or despite it, the ask on the future is falling relative to the bid on spot.

For now, let’s just say that the market is tight. The metal is out there, but obviously those who have it in an unencumbered form are not able (retail) or willing (others?) to take this backwardation bait.

I will drill deeper into this in another article soon.

Trackbacks & Pingbacks

[…] Around 25 cents per ounce. Yeah, backwardation is a concern. But this is nothing new, being just the new normal post 2008. But hey, let’s keep perpetuating the myth that only the paper price is going down. […]

Comments are closed.