There are but two ways that man can deal with man: reason and force. Reason includes invention, design, entrepreneurship, finance, borrowing and lending, construction, production, manufacturing, mining, farming, trade, marketing, distribution, sales, and contract.

Force is when someone picks up a gun. The gun is used to override the reason of the victim with the whims of the gun wielder. Criminals use force to steal and otherwise harm people. But criminals are only bit players. The main force-wielding actor is the government.

Economics is the study of people using reason to drive their activities, as listed above. Force is the negation of economics. There are several ways to see this.

How Force Negates Economics

One is that force attacks the mind. Those who act under compulsion, at gunpoint, are deprived at least partially of their use of reason. They may be aware of what they think is best, but this course of action will result in a bullet. So they take (at most) the second-best action. And often, those who are under duress experience some degree of mental paralysis as well. Especially over long periods of time, the mind trains itself to skitter away from the area of compulsion, like a bead of water on hot cast iron.

Two, force is not creative. It is destructive. Whereas people generally want to produce, save, conserve, accumulate capital, and live better, force pushes them to destroy, waste, eat the seed corn, and become impoverished. This is precisely why force is advocated by those who seek to wield it: to make people act in uneconomic ways.

Three, force causes economic discoordination. When spreads in the market become narrower, it means that coordination is increasing. Think of the spread between the price of eggs in a farm town and in a city 30 miles away. If people are able to coordinate their activities efficiently, there should not be a big price difference. But if you observe that the price of eggs in the city is a hundred times higher, that means that people are prevented from distributing eggs.

Whenever government uses force to interfere in markets, it promises improved outcomes. However, the opposite inevitably occurs. In my dissertation, I proved that every such instance causes wider spreads, and hence decreases coordination. The egg farmer earns less, and the city consumer pays more. Everybody loses.

Four, the follow-on effects cause economic retrogression. Farmers are ruined, and egg production is reduced. City workers go hungry for lack of eggs. Trucks that were purchased for egg distribution are wasted, possibly abandoned to rust or, at best, converted to a lower use. The scope of civilization is reduced.

Five, central planning prevents planning. In planning, people use reason to estimate their own needs and the needs of their customers. Then they budget resources, change their course of action, and take all steps appropriate to their plan. A central plan is when a bureaucrat dictates what shall be done, and what shall not be done. The people must obey because, the bureaucrat wields a gun.

Force is the negation of economics. The way poison or fire negates life. One could study the effect of fire on skin, seeking new treatments for those who suffer from burns. But one does not burn living animals while calling it “biology”.

And one does not force people to reduce the coordination of their productive activities, and call it “economics”.

What Happened to the Gold Standard?

This brings us to a December 16 article in The Economist, entitled “How Would the American Economy Have Fared Under a Gold Standard?” In one sense, this is amusing. The world began abandoning the gold standard on the eve of World War I. The US formed a central bank to begin interfering (by the use of force) in 1913. In 1933, it ended the domestic gold standard, preserving only redeemability for foreign governments. And that was ended in 1971.

Half a century ago, the last nail in the coffin of the gold standard was pounded into place. Yet The Economist bravely beats the dead body of the gold standard again.

Have they at least come up with a new argument, not used to rationalize the initial adulteration of the gold standard in 1913, not used to justify making the dollar irredeemable to Americans in 1933, and not used to sell us on the plunge into a worldwide regime of irredeemable currency in 1971?

Not quite.

The Economist simply declares that, “It requires Herculean assumptions for the gold standard to beat today’s regime…”

For all its pretense of looking back to WWI, The Economist does not seem to know about the prewar gold standard. There was no Federal Reserve. However, the article blithely asserts that a hypothetical gold standard today, ”…would have required the Fed to set interest rates to maintain a fixed dollar price of gold…”

Ack-tchu-uh-lee, no it wouldn’t.

The Herculean assumption of The Economist is that the government will always be forcing the economy via dictating interest rates. Under this assumption, the only debate is the method that the economic forcer should use to determine the interest rate.

A Lesson From the Soviets

Economists knew something even before the Soviet Union proved it ten-million-fold. If you try to centrally plan corn production, people die of malnutrition. Corn is a simple product. It has an annual cycle. You just put seed in the ground, wait for rain and sun, and harvest it. The Soviets killed tens of millions of people because they could not centrally plan corn.

After the mass-death caused by the Soviet experiment in central planning, even non-economists knew that central planning of corn is deadly.

Ignoring this lesson from history, if not economics, The Economist still believes that we can centrally plan credit. Credit is much more complicated, and it affects the production of everything in the economy. Unlike corn, the credit cycle is not fixed at one year. Its cycle is variable, ranging from years to decades.

Centrally-Planning Gold

So I must tell The Economist that the gold standard does not mean a different flavor of Fed-price-fixing scheme.

There is no right price of gold—but if even there were, a central planner would not know it. The right price is constantly fluctuating. More importantly, the mechanism for setting prices in a free market is different than the central planner’s administration. And it has different impacts on the economy, which feed back into numerous other processes and decisions. So even if the Fed could somehow divine the right price of gold in real-time, and somehow adjust interest rates in real-time so as to maintain this price, it would cause heaps of trouble all over the economy.

The Economist is right about one thing. Whatever the right process is, to set the price of gold, that process is not the Fed’s blunt instrument of interest rate policy.

The irredeemable currencies are failing, as we see with the final collapse of their interest rates. It makes little difference what monetary policy rule the central banks try to adopt. They have successfully waged their War on Interest. It’s over. Interest cannot be resuscitated now. For this reason, the world must move forward toward a new gold standard.

I close with some questions for The Economist. Do you want to cling to the failing fiat currencies and central planning model? Or are you interested in exploring what a vibrant free market in money and credit could and should be?

Are you interested in economics, or dirigisme?

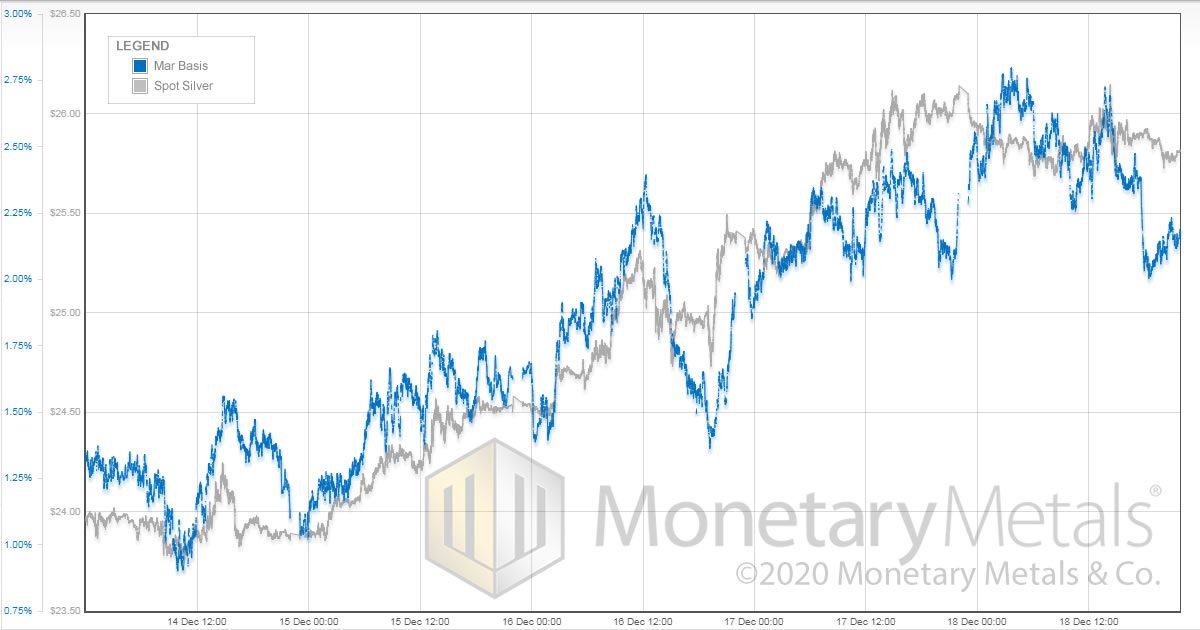

Recent Activity in Gold & Silver

Last week, the price of gold rose about $40 but the price of silver jumped about $1.80. That’s 7.5%.

Here are high-resolution graphs of the price and basis (i.e. fundamentals of supply and demand) in both metals for last week.

In gold, it looks like the basis wants to drop away from the price a few times, though it catches up in the end. A rising price with dropping basis means that the market is being moved by buyers of physical metal. But that last big surge in basis (over 50bps) around noon (London time) on Friday brings the basis in line with the same trend as at the start of the week. That is, futures buyers were obliged to step in to hold the price.

In silver, the basis and price lines are a better fit. That is, the futures buyers (and sellers) drove the price up (and down, during those moments when it went down).

We are reading more and more about the expectation of inflation. Even The Economist seems to be part of the consensus: the big increase in the quantity of the Fed’s liabilities will—at long last—cause prices to rise (plus The Economist says there will be a shortage of workers).

If people believe that prices will begin skyrocketing, what should they buy? Apparently, this week, the answer is gold to some degree, silver to a greater degree—and bitcoin to the greatest.

Bitcoin has now well over doubled, in less than three months. This is either a whole lot of inflation expectations crammed into one trade. Or else, it’s a whole lot of speculation blowing into one bubble.

On a private email list, we read one argument this week, that claimed gold and bitcoin are the “anti-fiat” assets. The rest of the debate was about which is going up faster. Obviously bitcoin. Therefore bitcoin is the better anti-fiat. QED.

We say, “wait a minute!” If you buy something because it’s going up in dollars, measure it in dollars, anticipate selling for more dollars, and count this gain of dollars as a gain of money, then perhaps this something is not “anti” dollar, but a “means of making dollars”.

The Economist is the property of the Rothschild. The people who succeeded to dominate the world by replacing gold with debt.

So we should not give them too much attention when they talk about gold.

Are you interested in economics, or dirigisme?

When you look at the technocracy the WEF is trying to implement, the answer is clearly dirigisme.

I was thrilled to see the link to Keith’s dissertation in the above. I’d read halfway through earlier, lost it somehow, and was unable to recover. Can hardly wait to dive back in. Great stuff, and so clear. Kinda reminds me of of an economy operating under the gold standard. Thank you.