Silver Is Now Offered At a Discount, Report 2 July, 2017

Have you ever been in a discussion about gold, when someone blurts out “we don’t have enough gold to operate a gold standard!” We have a standard retort. “Oh, that’s interesting. Please tell us how much gold you think would be necessary, and how you calculated it.”

We have never heard a coherent answer to this question. Most people just don’t like gold, and will say whatever words they think will dismiss the monetary question entirely, without actually having to address the issues.

The common answer from the gold community is not much better, “We could have a gold standard, if gold was at the right price.”

Here is the typical logic: divide the money supply by the amount of gold. The result tells you the price of gold to fully back the money supply. Let’s first use M1 (we are aware that which measure of money supply to use is debated, but we don’t think it much matters). M1 today is $3.5 trillion, according to the Fred Economic Data published by the St Louis Fed.

Divide this by the amount of gold. Often, this is supposed to be the amount of gold held by the Fed itself, some 8,133 tons or 261.5 million ounces. The answer comes out to $13,400 per ounce.

Or, you could take global M2 money supply of about $70 trillion and divide by total known gold stocks of 180,000 tons or 5.79 billion ounces, which is $12,000 per ounce.

It doesn’t work that way. Each ounce of gold is not a bucket, to collect its pro rata share of the dollar rainwater that falls out of the sky.

To use a historical anecdote as an analogy, the Medievals thought that if you throw a rock, it flies straight until it runs out of force, and then it turns the corner and falls straight down. It’s tempting, easy, simple, convenient—and wrong. Rocks do not fly that way. And the price of anything, including gold, is not set by dividing quantities.

This approach is based on an assumption, that every printed bank note is to be fully backed by the corresponding quantity of gold. However, it never worked like this historically. An honest bank is obligated to redeem its currency on demand, but that does not mean it would keep all that gold lying about in a vault. Why issue a currency, just to buy gold, store it, and incur costs?

This is a curious position for advocates of the gold standard to take. Money is still defined as the dollar. But money is to be backed by gold, which is not money (as money is the dollar)—so what does that make gold?

This stock goldbug answer—that the gold standard is just a matter of price—is transpicuous. In saying this, he shows that he just wants gold to go to $12,000 or more.

He wants to be rich, by front-running the herd. All those people will desperately need gold—come the day. And the goldbug plans to be there, parceling out his gold in exchange for the finest luxuries. He will readily part with it, when its purchasing power goes up by 10 times.

Needless to say, this is not an attractive vision of the future for most people. There are many reasons why they remain firmly in favor of central banks and against gold. This is one of them. So, if you want to win support for the gold standard, please don’t argue that gold will go up.

By the way, this is not a path to get to the gold standard anyways. It is true that, today, no amount of gold is enough. A few thousand tons are produced by the miners every year, but that is absorbed by the market. All new gold goes into hoards.

In the late 19th century, at the peak of the gold standard, the world’s monetary system and trade was run out of London. There were about 150 tons of gold in London at the time. Today, miners in just the state of Nevada produce 160 tons. Whatever it was that made the gold standard work, it was not an impossibly large quantity that we couldn’t hope to muster today.

A higher price will not bring gold into circulation. Gold did not circulate when its price was $250 in 1999, nor when it hit almost $2,000 in 2011. It will still not circulate if the price hits $15,000 in the future. High or rising prices will not do the trick. In the classical gold standard, it was not high price that did it.

This discussion of price begs a very serious question. What does price mean, if the money has a price measured in terms of something else? If the money is gold, then what is its price to be measured in? If gold is not the money, then what does gold standard mean? In our vision of the gold standard, gold is recognized as money, and prices are measured in terms of money, i.e. in terms of gold.

If it was not high price of gold, what was it that brought gold into circulation?

Interest.

Without interest, gold leaves the market. No amount is enough. Private hoards are a bottomless pit, as we see today. Without interest, why risk your gold by lending it? As to spending it, why spend gold when you can spend paper? People may be happy to be paid in gold, but no one wants to pay gold out.

But if interest is allowed to rise, then more gold is attracted into the market. Gold owners seek a return on their gold.

It may be urban legend—we have been unable to find the quote recently—that in one of the banking panics around the turn of the last century, someone approached John Pierpont Morgan. “There is a crisis in New York, a shortage of gold, what are we going to do?!”

“Raise the interest rate. 4% will draw it off the continent, and 5% will pull it down from the moon!”

At what rate would you be willing to lend your gold? Please tell us.

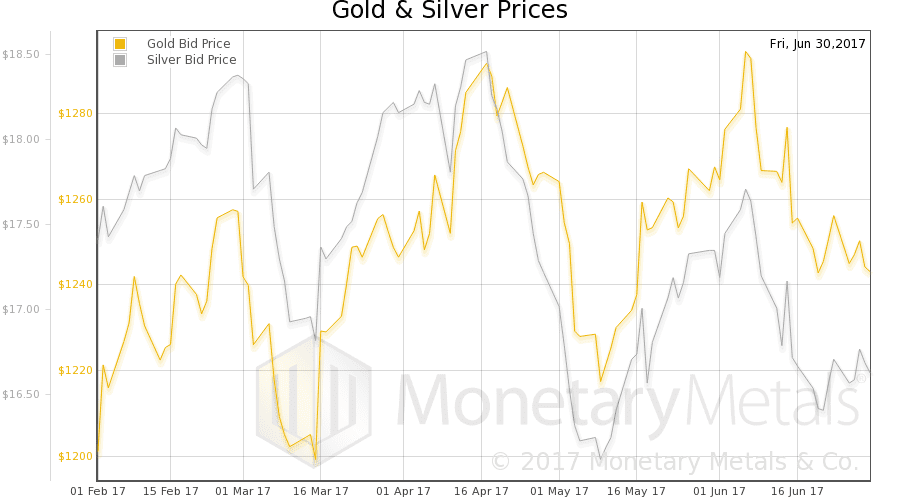

This week, the price of gold dropped $15, and that of silver 10 cents.

As always, we are interested in the fundamentals. The discussion above may inform one’s decision to own gold, but it is of no use in trading. Trading requires a picture of the current market conditions, the supply and demand conditions. Monetary Metals provides the only true measure of the fundamentals. But first charts of their prices and the gold-silver ratio.

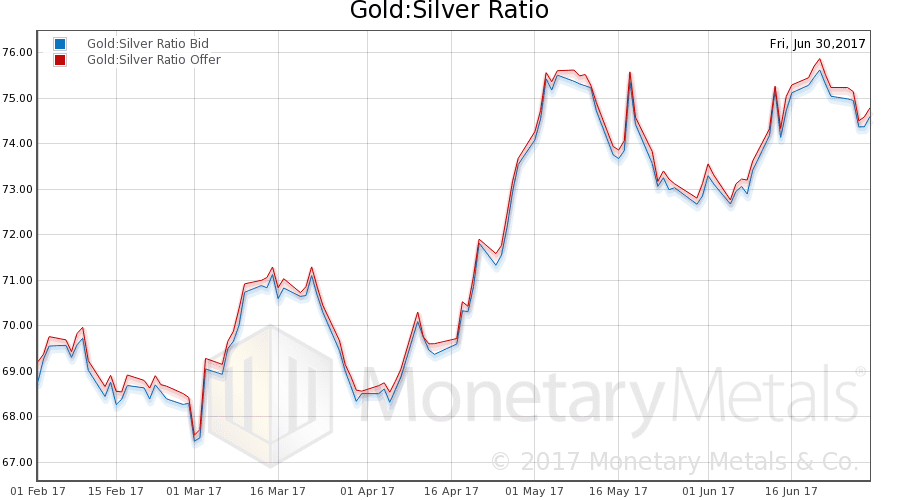

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio.

In this graph, we show both bid and offer prices for the gold-silver ratio. If you were to sell gold on the bid and buy silver at the ask, that is the lower bid price. Conversely, if you sold silver on the bid and bought gold at the offer, that is the higher offer price.

The gold-silver ratio fell slightly this week.

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

We had a rising price of the dollar (the mirror image of the falling price of gold). The abundance fell (the basis) and the scarcity rose (the cobasis). Funny how the cobasis likes to snap to zero, more often than random chance would dictate.

Our calculated gold fundamental price rose about $6 (chart here).

Now let’s look at silver.

The same pattern occurs in silver, rising scarcity. And the silver cobasis also hit 0.

Zero is an interesting number for the cobasis, because it’s the margin where decarrying becomes profitable. Decarrying is when you sell metal and buy a futures contract to recover the position. This trade does not require credit, only the metal.

Of course, as the metal trades the cobasis is constantly moving around. When someone bids up the futures contract, the cobasis subsides into negative territory. When the future is sold off, the cobasis rises. It crossed the zero line many times on Friday. When it is negative, there is no arbitrage opportunity. When it is positive, there is.

It should be interesting to see if the cobasis moves firmly into positive territory this week.

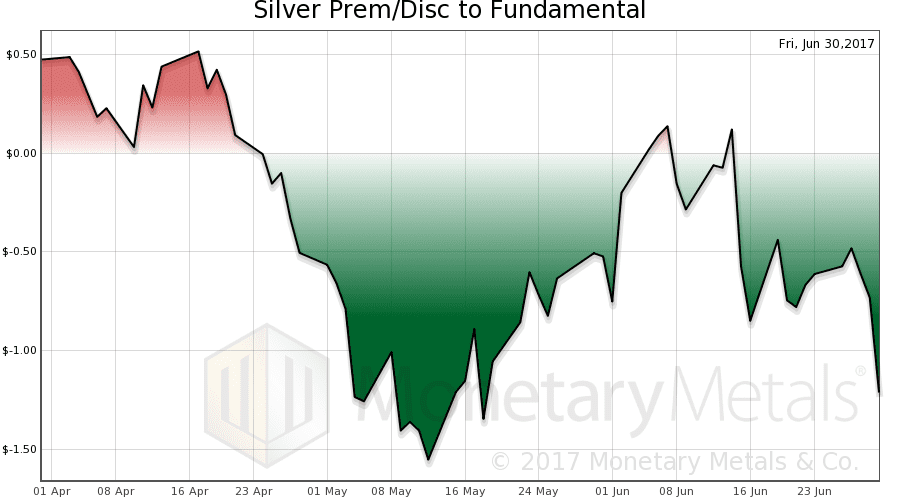

Our silver fundamental price increased $0.53 to $17.85. Here is a graph showing the discount (green) or premium (red) for silver.

The last time silver had such a large discount was the first week of May. After that, the price rose more than $1.25.

Monetary Metals will be exhibiting at FreedomFest in Las Vegas in July. If you are an investor and would like a meeting there, please click here.

© 2017 Monetary Metals

I bet today’s action (Monday) gives a positive cobasis. Anyway, it’s good to see the spec longs selling out. As you point out, that portends some bargains for the rest of us.

Nice work on the website lately… bravo! It’s all coming together.

Keith,

Your above discussion about gold, returning to a gold standard, circulating gold, and interest is one of the most profound essays that has been written in the gold sphere. You have outdone yourself. Keep ideas like that coming.