| Monetary Metals & Co. LinkedIn Profile | https://www.linkedin.com/company/monetary-metals-&-co./ | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. For more information, please visit monetary-metals.com. Founded in 2012 and headquartered in Scottsdale, Arizona, Monetary Metals is a different kind of gold company. Unlike others that simply buy or sell gold for dollar price appreciation, Monetary Metals unlocks the productivity of gold by matching investors who hold gold and silver with qualified precious metals businesses who need financing, including mints, refiners, jewelry manufacturers, miners, and recyclers. The businesses benefit from financing denominated in metal—which removes the need to hedge their price exposure—and owners of gold and silver can benefit from growing their total ounces of metal. The company offers two primary gold fixed income products: gold leases and gold bonds (gold bonds are for accredited investors only), which deliver income paid in physical ounces rather than dollars, eliminating storage fees and enabling investors to achieve compounding returns in ounces gained rather than mere dollar price appreciation. Since launching the Gold Yield Marketplace™ in 2016, the company has completed over 80 funded transactions across six continents. Monetary Metals has served thousands of clients—including family offices, high net worth individuals, and institutional investors— with the vision that everyone can save, earn and finance production in gold. |

| Monetary Metals & Co. X (Twitter) Profile | https://twitter.com/Monetary_Metals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform. |

| Monetary Metals & Co. Facebook Profile | https://www.facebook.com/MonetaryMetals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified businesses. |

| Monetary Metals & Co. YouTube Channel | https://www.youtube.com/c/Monetary-metals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. |

| Monetary Metals & Co. UAE Website | https://www.monetary-metals.ae/ | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified businesses. |

| Monetary Metals & Co. Inc. Profile | https://www.inc.com/profile/monetary-metals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace platform, by offering gold-denominated financing to qualified businesses. |

| Monetary Metals & Co. Pitch Book Profile | https://pitchbook.com/profiles/company/155796-94 | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified businesses. |

| Monetary Metals & Co. Tracxn Profile | https://tracxn.com/d/companies/monetary-metals/__tWpXFqZV_Ax5kTWcCI_QekEMBATS_E_6yIVgznl7OwM | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace platform, by offering gold-denominated financing to qualified companies in the precious metals industry. |

| Monetary Metals & Co. Better Business Bureau (BBB) Profile | https://www.bbb.org/us/az/scottsdale/profile/investment-management/monetary-metals-1126-1000087817 | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified businesses. |

| Monetary Metals & Co. Crunchbase Profile | https://www.crunchbase.com/organization/monetary-metals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing. |

| Monetary Metals Google Patents Profile | https://patents.google.com/?assignee=Monetary+Metals+%26+Co | Google patents profile for Monetary Metals as an assignee |

| Monetary Metals Google Business KGMID | https://www.google.com/search?kgmid=/g/11vldcrgw9 | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. |

| Monetary Metals alternative name (Monetary Metals Corp) KGMID | https://www.google.com/search?kgmid=/g/11f01bkd18 | The KGMID associated with Monetary Metals Corp, an alternative name for Monetary Metals & Co. |

| Monetary Metals & Co. Trustpilot profile | https://www.trustpilot.com/review/monetary-metals.com | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified businesses. |

| Monetary Metals & Co. Bloomberg company profile | https://www.bloomberg.com/profile/company/1627759D:US | Monetary Metals & Co. delivers a yield on gold, paid in gold, via its Gold Yield Marketplace platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding overtime with no storage fees. |

| Monetary Metals & Co. bitscale.ai profile | https://bitscale.ai/directory/monetary-metals-and-co | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. For more information, please visit monetary-metals.com.

Founded in 2012 and headquartered in Scottsdale, Arizona, Monetary Metals is a different kind of gold company. Unlike others that simply buy or sell gold for dollar price appreciation, Monetary Metals unlocks the productivity of gold by matching investors who hold gold and silver with qualified precious metals businesses who need financing, including mints, refiners, jewelry manufacturers, miners, and recyclers. The businesses benefit from financing denominated in metal—which removes the need to hedge their price exposure—and owners of gold and silver can benefit from growing their total ounces of metal. The company offers two primary gold fixed income products: gold leases and gold bonds (gold bonds are for accredited investors only), which deliver income paid in physical ounces rather than dollars, eliminating storage fees and enabling investors to achieve compounding returns in ounces gained rather than mere dollar price appreciation. Since launching the Gold Yield Marketplace™ in 2016, the company has completed over 80 funded transactions across six continents. Monetary Metals has served thousands of clients—including family offices, high net worth individuals, and institutional investors— with the vision that everyone can save, earn and finance production in gold. |

| Monetary Metals & Co. PR Newswire profile | https://www.prnewswire.com/news/monetary-metals-%26-co./ | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. |

| Monetary Metals & Co. Rocket Reach Profile | https://rocketreach.co/monetary-metals-co-profile_b44cf87bfd5765aa | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. For more information, please visit monetary-metals.com. |

| Monetary Metals & Co. privco.com profile | https://www.privco.com/company/monetary-metals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. |

| Monetary Metals & Co. CB Insights profile | https://www.cbinsights.com/company/monetary-metals | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions earn a yield on gold and silver every month, compounding their holdings over time without storage fees. It was founded in 2012 and is based in Scottsdale, Arizona. |

| Monetary Metals & Co. Bullion.Directory listing | https://bullion.directory/bullion-dealers/monetary-metals-reviews/ | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified companies in the precious metals industry. Through its gold leases and gold bonds, investors and institutions worldwide earn a yield on gold and silver every month, compounding their holdings over time with no storage fees. For more information, please visit monetary-metals.com.

Founded in 2012 and headquartered in Scottsdale, Arizona, Monetary Metals is a different kind of gold company. Unlike others that simply buy or sell gold for dollar price appreciation, Monetary Metals unlocks the productivity of gold by matching investors who hold gold and silver with qualified precious metals businesses who need financing, including mints, refiners, jewelry manufacturers, miners, and recyclers. The businesses benefit from financing denominated in metal – which removes the need to hedge their price exposure – and owners of gold and silver can benefit from growing their total ounces of metal.

The company offers two primary gold fixed income products: gold leases and gold bonds (gold bonds are for accredited investors only), which deliver income paid in physical ounces rather than dollars, eliminating storage fees and enabling investors to achieve compounding returns in ounces gained rather than mere dollar price appreciation. Since launching the Gold Yield Marketplace™ in 2016, the company has completed over 80 funded transactions across six continents. Monetary Metals has served thousands of clients – including family offices, high net worth individuals, and institutional investors – with the vision that everyone can save, earn and finance production in gold. |

| Monetary Metals & Co. Instagram profile | https://www.instagram.com/monetary_metals/ | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to companies. |

| Monetary Metals & Co. TikTok profile | https://www.tiktok.com/@monetarymetals | Monetary Metals delivers a yield on gold, paid in gold. |

| Monetary Metals & Co. Wikidata entry | https://www.wikidata.org/wiki/Q139589172 | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing. |

| Monetary Metals & Co. OpenCorporates profile | https://opencorporates.com/companies/us_de/5166254 | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing. |

| Monetary Metals & Co. LEI Identifier | https://search.gleif.org/#/record/254900N6I62WNJ1VT195 | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing. |

| Monetary Metals & Co. Primary KGMID | https://www.google.com/search?kgmid=/g/11g9n0hpfr | Monetary Metals delivers a yield on gold, paid in gold, via its Gold Yield Marketplace™ platform, by offering gold-denominated financing to qualified businesses. |

Perfect explanation.

Keith, agree with the view. However, where one funding source vacates another one takes its place. There are more angel investors / venture capitalists now because they are willing to take on higher risk in exchange for higher reward.

The side effect to a ultra low interest rate environment which I observed, and personal opinion is the speed of change / innovation cycle have sped up. In the past new innovations will enjoy a good number of years recouping ther cost plus reaping the profits but nowadays they have a much shorter cycle and have to constantly stay on the edge.

There’s a equilibrium and yet almost a vicious cycle that spirals downwards. I wonder when it will ever stop.

Yuhanni: I think the angels and VCs have been in a process of moving away from risk, which began after 2001. Today there are more angels I am sure, but they’re pretty picky about deals. To the point of this article, angles are not typically interested in financing a restaurant, factory, car dealership, or the like.

And of course angel capital is extremely expensive to the entrepreneur. While the large corporation is gorging on credit it can have for the low cost of 100 basis points or so, an entrepreneur has to give up a third or more of the equity in his company. The large corporation can use the proceeds to enrich management by buying back shares, driving the price up, and triggering executive bonuses tied to stock performance. The entrepreneur may not be able to use the proceeds even to pay himself a salary.

Yuhanni, in my industry, venture capital has been scarce for the past 10 years. There are a couple of factors involved. First, my industry (Electronic Design Automation) is relatively mature in the high tech sector. However, more importantly, VCs want to put their money into social media startups due to the perceived payback. If a VC invested $10M in an EDA startup, they’d be extremely lucky to get 3-5x on their money in 10 years. That much money in a social media startup could return 10-100x in less than 10 years. (Historically. I think that era is just about over.) This is surely due more to the mania in social media stocks than anything else. However, money goes where the promise for return is biggest.

Meanwhile, we are left to contemplate why millions and billions are going into social media which has a spotty record of actual productivity gains and seems to gain most of its value by obsoleting old-style advertising (shifting revenue from an established bucket to another bucket, not growing the bucket). The productivity gains are real, but very hard to measure. For those old enough, how much more do you get done today given that 50% of your work day or more (certainly true for many people in my industry) is consumed with email reading and responding? Yeah, all that information is worth something, but half a person’s day in productivity every day? On the other hand, my industry is critical to enabling the semiconductor industry, which generates >$100B/year. Without EDA, there could not have been Moore’s Law (2x increase in function and speed every 18-24 months) in computers, enabling smartphones, tablets, the internet, etc. That is real and relatively easily measurable productivity. Yet, VCs don’t want to touch startups in EDA.

I’ll give one example. It is my job to analyze and direct my division into new technology areas. As a result, I talk to startups and evaluate whether they have anything worth acquiring. One that I talked to recently is working in an area of interest. We already did one acquisition that puts us into that same market. However, this startup has ~$10M in VC funding. In order for a large EDA company to acquire a startup for an amount that pays back the investors (0 return), the startup must achieve on the order of $30-50M in annual revenue. That would take years to achieve even with a standout product and good marketing/sales. I cannot comment on whether they have a standout product. The finances are such that it isn’t worth our time to do the due diligence. I expect this company to fail. It makes no sense for the investors to put more money into this startup. They’ll try to sell it off. Without adequate revenue and no funds to build a sales force to generate it, the VCs are looking at getting <$0.50 of every $1 they put into this startup.

Sure, there are situations where the investors could've gotten back their investment and maybe a bit of a return. But, this example shows that something's broken in this industry. It isn't particular to this one startup company. The VC risk-reward analysis is upside down.

Another example is a networking startup that has ~$160M invested. Will this company generate a return for its investors? In this case, it is possible. They appear on the verge of reinventing how network chips are designed and implemented. But, this is a different industry from EDA. It is networking. VC funds are still flowing to semiconductor companies (the customers of EDA), but not as much as social media and the heyday of the 1990's.

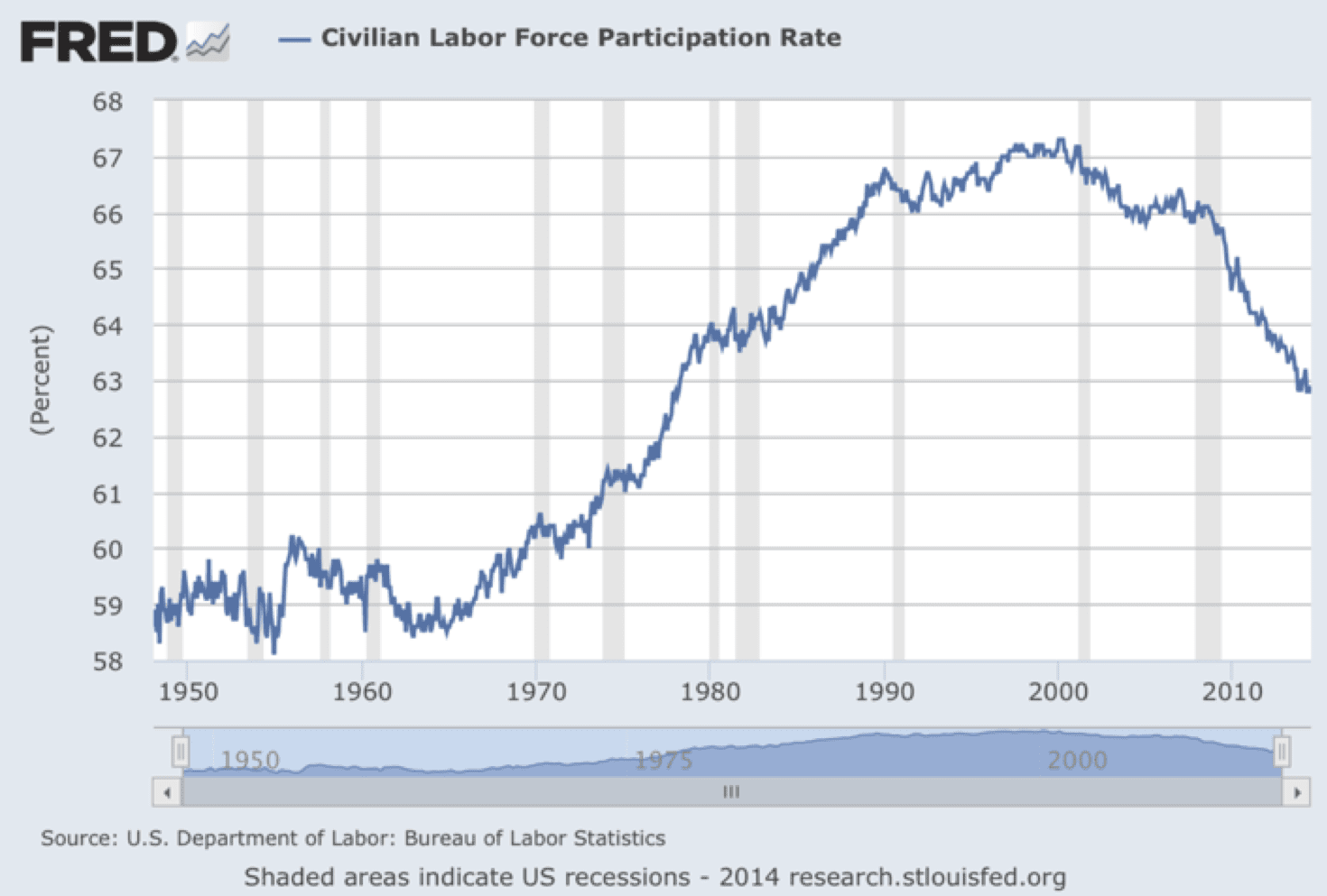

Keith – I’ve been enjoying your newsletters for some time now and I really respect your insight and opinions. I do wonder about a few things in this particular commentary. I’m not sure I understand why newer businesses are “dehydrated.” It seems they’d have little trouble issuing debt since people are buying lower and lower rated bonds to get the higher interest. I also wonder if the aging population would account for a good share of the decrease in the labor force participation rate due to retirement or the choice to reduce hours?? Thank you for all your wonderful commentaries.

Update: I see the participation rate refers to working age.

bvigorda: The typical startup does not have access to the bond market. At best, it can borrow from a bank, and the bank might be able to securitize the loan and sell off a pool of such loans into the bond market (if the regulators allow it).

Thanks Keith!

Very few can write the way you do Keith. Thank you , your explanations are always very concise and genius !